Cristhian Rêgo Passos - E-mail: cristhianpassos@yahoo.com.br, Orcid: https://orcid.org/0000-0002-7965-9718, Afiliação Institucional: Universidade Federal do Piauí - Teresina Brasil

Guiomar de Oliveira Passos - E-mail: guiomar@ufpi.edu.br, Orcid: https://orcid.org/0000-0002-6106-4900, Afiliação Institucional: Universidade Federal do Piauí – Teresina – Brasil

Resumo

Este texto analisa a arrecadação de impostos de competência municipal no contexto fiscal no período de 2003 a 2019, traçando o panorama atual da receita proveniente desses impostos, segundo a região, o porte populacional, a categoria (se capital ou interior) e a participação de cada imposto nos agrupamentos considerados. Utilizou-se pesquisa bibliográfica e a base de dados disponibilizada por Santos, Mota e Faria (2020), analisada por de medidas de frequências absolutas e relativas e coeficientes de variação. Constatou-se que a arrecadação mais que dobrou no período, sendo os municípios mais populosos e com maior participação no PIB nacional, geralmente localizados na região Sudeste, os que arrecadam mais, e o Imposto Sobre Serviços (ISS) é que mais contribui em todos os grupos, refletindo a natureza urbana da base tributária municipal, cada vez mais assentada, ao passar dos anos, no setor de serviços, cuja cobrança representa menores custos administrativo e político.

Palavras-chave: Arrecadação municipal de impostos. Competência tributária municipal. Receitas municipais.

Abstract

This text analyzes the collection of municipal taxes in the fiscal context in the period 2003 to 2019, tracing the current panorama of revenue from these taxes, according to region, population size, category (capital or interior), and participation of each tax in the considered groups. Bibliographic research and the database provided by Santos, Mota, and Faria (2020) were used, analyzed by measures of absolute and relative frequencies and coefficients of variation. It was found that the collection more than doubled in the period, with the most populous municipalities with the largest share of the national GDP, generally located in the Southeast region, the ones that collect more, and the Tax on Services (ISS) is the one that contributes the most in all the groups, reflecting the urban nature of the municipal tax base, increasingly settled over the years in the service sector, whose collection represents lower administrative and political costs.

Keywords: Municipal tax collection. Municipal tax jurisdiction. Municipal revenues.

The 1988 Constitution of the Federative Republic of Brazil (CRFB/1988) elevated municipalities to members of the federation, granting them, as the states, administrative, political, and financial autonomy. The political-administrative autonomy gave them the capacity for self-organization, self-government, self-administration and self-legislation, and the financial autonomy gave them the competencies to tax, spend, and incur debts (AFONSO, 2007). The Fiscal Responsibility Law (Complementary Law No. 101/2000), in turn, established, as one of the duties "in fiscal management, the institution, forecast and effective collection of all taxes of constitutional competence" of each entity of the Federation (BRASIL, 2000), constituting a vital enforcement mechanism for all of them.

This article analyzes the collection of municipal taxes in the fiscal context after the 1988 Federal Constitution; in a way, it verifies the fulfillment of one of the duties in fiscal management provided in Complementary Law 101/2000, because it examines what was collected by the municipalities through the taxes that concern them. The collection analyzed here comprises the revenue from ISS, IPTU, and ITBI, i.e., the taxes whose competence was constitutionally attributed to the local sphere of government. The question is: What is the tax collection of Brazilian municipalities? How did municipal tax collection evolve from 2003 to 2019? How is the collection of municipal taxes distributed among the geographic regions? Which region collects the most taxes? Which municipal tax has the largest share among those that fall under municipal jurisdiction? What types of municipalities collect the most taxes?

What is investigated is how much the municipalities collected through taxes in the period from 2003 to 2019, tracing the current panorama of this revenue according to region, population size, category, and composition in each of the groupings considered. This is a systematization effort driven by two intentions. The first is instrumental: we seek to identify what has been collected by Brazilian municipalities to subsidize the investigation of the effects of strengthening the taxation capacity of this government sphere brought about by the 1988 Constitution. The second is theoretical and practical in the sense that Weber (2006) attributed when he dealt with objectivity in the social sciences: we seek facts, that is, data on the reality of the municipalities' tax collection in order to contribute to the debate about the gains of this sphere with the fiscal design established in the 1988 Constitution, as well as the limitations of part of them, those with less than 5 thousand inhabitants, to collect at least 10% of their total revenue.

Therefore, it focuses on the collection of taxes under the competence of municipalities, not establishing a comparison between this and the taxes collected by other entities, nor does it verify what this represents as total tax collection, even though this approach is relevant and has been addressed by Tristão (2003), Orair and Alencar (2010), Massardi and Abrantes (2015), and Suzart, Zuccolotto, and Rocha (2018). However, what is being examined is what municipalities do with the financial autonomy granted to them by the Constitution or, in other terms, how they have exercised the duty of collection in fiscal management.

The theme, object of legislative actions, examples of which are the Proposals for Constitutional Amendments nº 45/2019 and nº 110/2019 (BRASIL, 2019a) and nº 188/2019 (BRASIL, 2019b), is also the main theme by many scholars. Some, like Serra and Afonso (1999), after outlining the diagnosis of the Brazilian federation in the first ten years after the 1988 Federal Constitution, pointed out its challenges and perspectives, indicating the necessary reforms. Others weave the diagnosis of municipal tax collection capacity (AFONSO; ARAÚJO, 2000), analyzing the evolution and behavior of municipal tax collection (BREMAEKER, 1994; TRISTÃO, 2003), measuring their tax effort (ORAIR; ALENCAR, 2010; MASSARDI; ABRANTES, 2015; SIQUEIRA; PAES; LIMA, 2016) or their tax efficiency (FERNANDES, 2017). All of them offer elements to expand the knowledge about "the role of municipalities in the Brazilian fiscal debate" (AFONSO et al., 1998, p. 3) or even about the complexity of the Brazilian federation.

This paper, while presenting a current diagnosis of tax collection in municipalities, continuing the efforts started by Afonso et al. (1998) and joining the updates undertaken by, among others, Afonso and Castro (2018, 2019), analyzes the participation of each tax in the total revenue, according to geographic regions, population, and location of municipalities

For that, it is used the Single Base for Municipal Tax Collection data built by Santos, Mota, and Faria (2020, p. 2) due to the discrepancies and inconsistencies of the three existing bases: Information System on Public Budgets in Health (SIOPS), under the responsibility of the Ministry of Health; Information System on Public Budgets in Education (SIOPE), under the responsibility of the Ministry of Education; and the database Brazil Finance - Accounting Data of Municipalities (FINBRA), under the responsibility of the Ministry of Economy through the National Treasury Secretariat (STN).

These data, already updated at May 2020 prices by the National Wide Consumer Price Index (IPCA) by Santos, Mota, and Faria (2020), were organized by region, population and location (capital or interior) of the municipalities, and submitted to statistical analysis using absolute and relative frequency measures and coefficients of variation.

The paper has four parts, including this introduction, which is the first. The second part outlines the tax competencies of Brazilian municipalities after the 1988 Federal Constitution. The third part exposes the collection of taxes of municipal competence as of the Federal Constitution of 1988, analyzing its evolution from 2003 to 2019 and its distribution according to regions, by type of tax and municipality. In the last section, the conclusion, is the current panorama of tax revenues from municipal taxes is outlined, showing how these federative entities exercise their tax powers.

Taxation is how the State maintains the operation of public services and provides investments. As Hamilton, Madson, and Jay (1993, p. 232) have already said, "Taxation is what sustains its life and movements, allowing it to perform its most essential functions."

In the Brazilian Tax System, each entity has powers defined by the Federal Constitution so that there are taxes specific to each level of government and a system of revenue sharing and intergovernmental transfers of tax resources, justified by the inequality in collecting capacities among the federation entities.

Municipalities are supported both by the taxes they collect and the parts of taxes collected by other entities passed on to them through mandatory or voluntary transfers. Mandatory transfers are those provided for in the Federal Constitution, and voluntary transfers are those made for the maintenance of agreements or consortia entered into between the subnational entity and the Union or between subnational entities for the execution of a work or service provision (SUZART; ZUCCOLOTTO; ROCHA, 2018).

The municipalities' collection, as provided for in the Constitution, occurs through the collection of taxes on urban territorial property, the provision of services, the disposal of real estate, as well as through the collection of fees for the exercise of police power, or the provision of services and through the collection of improvement contributions, due to works or improvements performed by the municipal administration on public roads that bring direct or indirect benefits to taxpayers (ALEXANDRE, 2016).

The collection of urban territorial property takes place through the Urban Property Tax (IPTU), established by Article 156 of CRFB/1998 and regulated by the reception of articles 32 to 34 of the National Tax Code (CTN) - Law No. 5172 of October 25, 1966. Its taxable event, in the expression of art. 32 of Law No. 5172/1966, is "[...] the ownership, useful domain or possession of real estate by nature or by physical accession, as defined in the civil law, located in the urban area of the Municipality" (BRASIL, 2017a, p. 17).

This tax is levied on the individual who holds possession with animus dominus, i.e., who acts as the owner, either by ownership or only by possession of real estate located in the urban area, which, as defined by municipal law, meets, according to the provisions of § 1 of Article 32 of the CTN, "at least 2 (two) of the following items, built or maintained by the Public Power":

I – curb or sidewalk, with rainwater channeling;

II – water supply;

III – sanitary sewage system;

IV – public lighting network, with or without poles for home distribution;

V – elementary school or health post at a maximum distance of three (3) kilometers from the property considered (BRASIL, 2017a, p. 64-65).

The calculation basis of the IPTU is, according to the provisions of article 33 of the CTN, the property's market value defined in the municipal generic plant by a reference (value per square meter) related to all properties in the region. The venal value is calculated through a real estate appraisal performed by technicians of the municipal treasury departments following all the technical requirements established in Ordinance No. 511 of December 7, 2009, of the Ministry of Cities (BRASIL, 2009).

The municipal collection of taxes on the sale of real estate is done through the Tax on Transmission of Real Estate "inter vivos" (ITBI). The tax levied by the municipality where the property is located is provided for in article 156 of the Brazilian Federal Constitution/1988, and regulated by articles 35 to 42 of the National Tax Code (CTN).

The ITBI tax is levied on any of the parties involved in the onerous transfer of real estate based on the property's commercial value, as specified by municipal law, which will also determine the tax rate. The taxable event, according to art. 35 of the CTN, is "the inter vivos transmission, for any reason, for valuable consideration, of real estate, by nature or physical accession, and rights in rem on real estate [...]" (BRASIL, 2017a, p. 22).

The municipal collection of taxes on the provision of services occurs through the Tax on Services of Any Nature (ISS). This is a tax present in the constitutional order, according to Harada (2014), since the Constitution of 1891, first of competence of the states, and then, with the Constitution of 1946, gradually transferred to the municipalities.

The transfer to the municipal sphere was consolidated with the 1965 Tax Reform, carried out by Constitutional Amendment No. 18 of December 1, 1965. This constitutional amendment granted municipalities the power to institute taxes on services of any nature, excluding those under the jurisdiction of the Union and the states, requiring, however, as of the 1967 Constitution, regulation and listing of services in a complementary law (HARADA, 2014).

The Federal Constitution of 1988 maintained the municipal competence to collect the ISS (art. 156, III; BRASIL, 1988), as well as the requirement for regulation by Complementary Law, ensuring, however, the regulations established by Decree-Law No. 406, of December 31, 1968 (BRASIL, 1968), until 2003, when Complementary Law No. 116 was published on July 31, 2003, to take effect as of the fiscal year 2004 (BRASIL, 2003), subsequently amended by Complementary Law No. 157, of December 29, 2016 (BRASIL, 2017b).

Law No. 116/03 determined that the ISS is levied on the value of the services described in the attached list of the aforementioned legislation, and the charge is made to the service provider - companies or independent professionals who perform any taxable service, i.e., specified in the legislation. The rates vary from 2% to 5% on the value of the services rendered and the collection is made, according to article 4 of Complementary Law 116/03, wherever they occur permanently or temporarily.

The collection of these taxes, in the context post-Constitution of 1988, particularly in the period from 2003 to 2019, is the subject of the next part.

This item exposes the tax collection of Brazilian municipalities under the 1988 Constitution, focusing first on the volume of resources calculated from 2003 to 2019 and then tracing its evolution over the period both in terms of growth and the share of taxes by geographic region, size, and type of municipality.

The context is the institutionality conferred on municipalities, first by the New Constitutional Charter of 1988, and then by the Fiscal Responsibility Law (Complementary Law No. 101/2000). From one, the financial autonomy, in which their tax powers are included, a scope in which, according to Afonso (2016, p. 24), "never in the Brazilian federative history have municipalities had such a large relative weight in the distribution and application of tax and public resources in general." On the other, the rules to act responsibly and zealously in the collection.

Indeed, the volume collected by the municipalities through the taxes of their competence, updated at current prices of May 2020, totaled in 2003, R$ 54,365,623,216.47 and in 2019, R$ 135,167,685,832.19 (SANTOS; MOTTA; FARIA, 2020), a period in which they experienced an accumulated growth of 148.6%, equivalent to an average annual growth rate of 6%, showing that they have developed their tax collection and management capabilities as established by the Fiscal Responsibility Law.

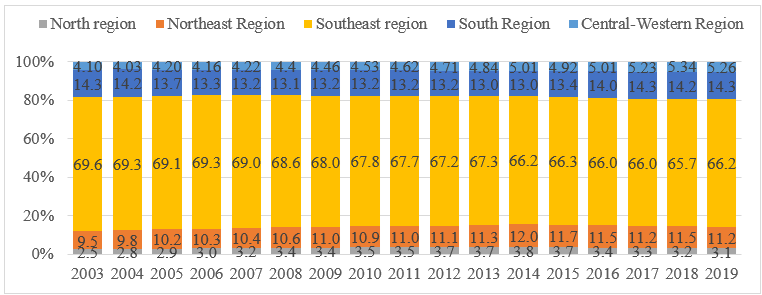

This growth, it is true, is not the same among the municipalities because, as Afonso, Araújo, and Nóbrega (2013, p. 13) pointed out, they are heterogeneous, "both in terms of their size and socioeconomic reality, and in terms of the means available to them to exercise their taxing power. This heterogeneity is reflected in the collection of taxes (IPTU, ISS, and ITBI), as can be seen in the regional distribution presented in Graph 1, in which the Southeast region (1,668 municipalities) participates with 66.2% to 69.6% of the total municipal tax revenues of the country, while the Northeast region (1. The North Region, which has 450 municipalities, participates with 2.5% to 3.8%; the South Region participates with percentages between 13% and 14.3%; and the Center-West with 4.03% to 5.34%.

Graph 1 – Percentage of tax collections of municipal competence (IPTU, ITBI, and ISS) by Region (2003 to 2019)

Source: Elaborated by the authors based on data from Santos, Motta, and Faria (2020).

The Southeast suffered a reduction of 3.4 percentage points in participation in the national tax collection, going from 69.6 to 66.2. The South Region oscillated between 14.2% in 2003 and 2004, 13% from 2005 to 2015, and 14% from 2016 to 2019. The North, Northeast, and Midwest regions increased their participation: the North from 2.5% to 3.1%, the Northeast from 9.5% to 11.2%, and the Midwest from 4.1% to 5.26%.

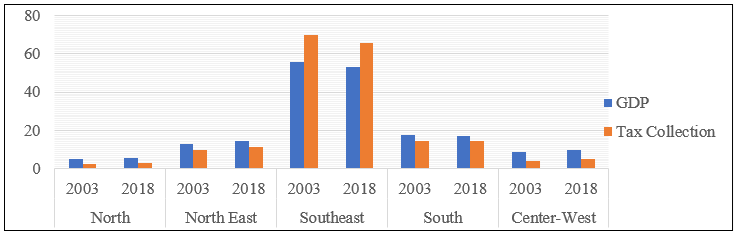

The participation in tax collection, as seen in Graph 2, follows the share in the production of wealth measured by the GDP. The set of municipalities with the most significant presence in the composition of the national GDP boasts greater participation in the collection of municipal taxes, so the set of municipalities in the Southeast Region, according to data from the IBGE's System of National Accounts (2020), contributed the largest share to the formation of the national GDP (55.8% in 2003 and 53.1% in 2018) and in the total tax collection (69.6% and 65.7%), and those with the lowest participation, the set from the North Region, participated with the most minor (4.8% and 5.5% of the national GDP; 2.5% and 3.2% of the collection).

Graph 2 - Percentage participation of each geographic region in the national GDP and in the total collection of municipal taxes (2003 and 2018)

Source: Elaborated by the authors based on IBGE data (2008, 2020).

Note: [2018] [2018] Last year with data on GDP per Region, made available by IBGE (2020).

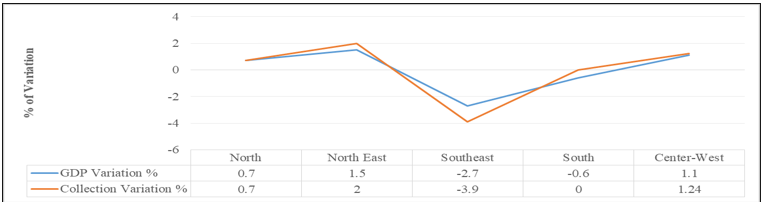

The participation in tax collection, along the analyzed period, as shown in Graph 3, follows the share of contribution in the composition of the national GDP, both when there is a reduction, in the case of the Southeast and South regions, and when there is an increase, as occurred in the North, Northeast, and Center-West regions. In the first group, the Southeast region reduced its participation in the national municipal collection by 3.9 percentage points, from 69.6 to 65.7, and 2.7 percentage points in its share in the national GDP, and the South region decreased by 0.6% and 0%. In the second group, GDP and tax collection grew, even in equal percentages, as in the North, 0.7 pp from 4.8% to 5.5%, or very close, in the Northeast, 1.5 pp, from 12.8% to 14.3%, and in the Center-West from 8.8% to 9.9%.

Graph 3 – Percentage variation in national GDP and municipal tax collection by Region between the years 2003 and 2018

Source: Elaborated by the authors based on IBGE data (2008, 2020).

The link between tax collection and the GDP reflects the municipal tax base that is increasingly based, over the years, on the services sector, which is currently the most important in the GDP composition (IBGE, 2020). In 2002, this sector represented 50.7% of added value to the national GDP and, in 2018, 55.6%. The municipal collection with ISS, which is the tax on taxable services, according to Complementary Law No. 116 of July 31, 2003, according to data from Santos, Mota, and Faria (2020), totaled, in 2003, R$ 23,929,960,234.43 and in 2018, R$ 67,510,177,531.51, representing, respectively, 1.13% and 0.94% of the national GDP. These percentages are higher than the 1.11% and 0.66% of the IPTU and the 0.18% and 0.17% of the ITBI.

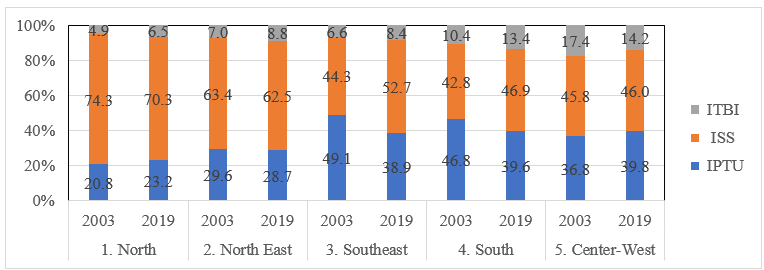

ISS, in 2003, as shown in Graph 4, was already the most significant municipal tax collection in the North, Northeast, and Center-West regions; and, in 2019, in all of them, representing, at the beginning of the period, 42.8% of the collection in the South region and 74.3% in the North region and, in the end, 46% in the Center-West and 70.3% in the North region. In the same period, the IPTU offered 20.8% of the tax revenue of the municipalities in the North region and 49.1% in the Southeast, 23.2% in the North region, and 39.8% in the Center-West. ITBI, on the other hand, varied from 4.9% to 6.5% in the North Region, and from 17.4% to 14.2% in the Middle-West Region.

Graph 4 – Percentage of municipal collection by type of tax according to geographic region (2003 and 2019)

Source: Elaborated by the authors based on data from Santos, Motta, and Faria (2020).

The participation of ISS in the total municipal collection most frequently represents the largest share of taxes; the exceptions are the percentages in the Southeast and South regions in 2003. On the one hand, this demonstrates its importance for municipal revenues; on the other hand, it highlights the focus of taxation on services to the detriment of property (IPTU). One, as observed Afonso, Araújo, and Nóbrega (2013, p. 70-71), is levied indirectly, not burdening "any specific segment of society"; the other is levied directly on taxpayers who "usually pressure the public authorities, in the sense of minimizing their obligations with the tax authorities," require "approval by the City Council and require the assembly of a collection structure, consequently, implying political and administrative costs."

As a result, the IPTU lost its tax collection primacy not only in the South and Southeast regions but also started to represent less than 39.8% in other regions. ITBI, which increased its share in tax collection in all regions except the Center-West, whose share fell by 3.2 pp, had its share increased in the other regions in the comparison between 2003 and 2019, by 1.8 pp in the Northeast, 1.6 pp in the North, 1.8 pp in the Southeast, and 3 pp in the South, respectively.

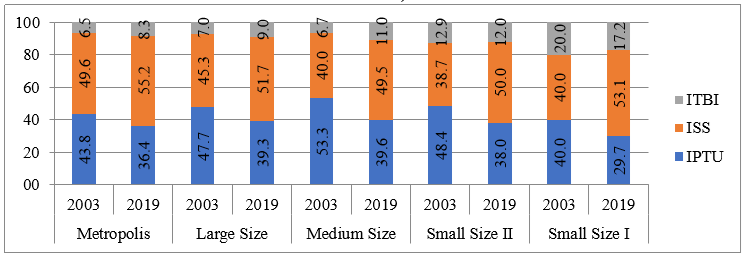

As Bremaeker (1994) has stressed, all of these taxes are urban, and as a consequence, they suffer the effects of factors such as population size. The Metropolises (the 17 municipalities with more than 900 thousand inhabitants), as shown in Graph 5, both in 2003 and in 2019, had the ISS as the tax with the highest share in the total collection. The others that initially had the IPTU reaching 48.4% in the 1,043 Small Size II (from 20,001 to 50,000 inhabitants) have all now ISS as the most collected tax, reaching 53.1% among the 3,919 Small Size I (up to 20,000 inhabitants), a percentage that is just below that of the Metropolises.

Graph 5 – Percentage of participation of each tax in the total tax collection according to the size of the municipalities (2003 and 2019)

Source: Elaborated by the authors based on data from Santos, Motta, and Faria (2020).

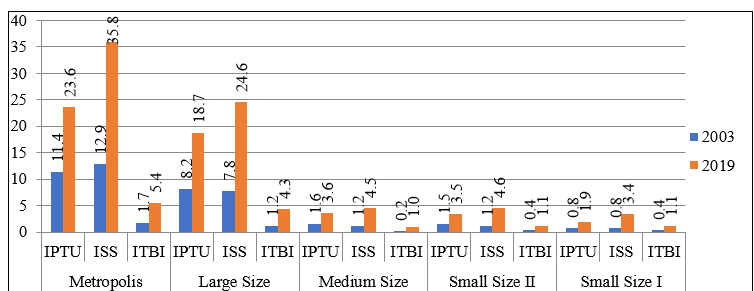

The ITBI increased its participation in the most populated groups and decreased in the smallest, especially in the tiny ones, in which this tax no longer contributed with 20.0% of the collection, but 17.2%. This, as shown in Graph 6, did not remove the ISS and the IPTU as the largest sources of municipal tax collection, the latter being the largest, in 2003, in the large, medium and small municipalities and the latter prominent, in 2019, among the metropolises, as it was in 2003, and in all other segments.

Graph 6 – Municipal collection by type of tax in billions (R$) according to the size of the municipalities (2003 and 2019)

Source: Elaborated by the authors based on data from Santos, Motta, and Faria (2020).

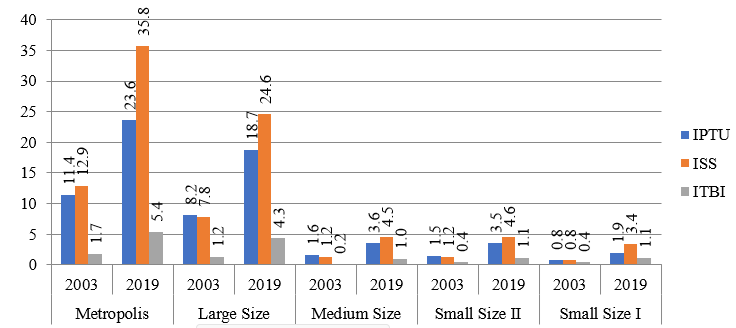

The collection of all municipal taxes, as shown in Graph 7, grew between 2003 and 2019 in all types of municipalities. In the Metropolises, in billions of reais, IPTU increased from 11.4 in 2003 to 23.6 in 2019, ISS increased from 12.9 to 35.8 and ITBI from 1.7 to 5.4; in the Large-sized ones, IPTU increased from 8.2 to 18.7, ISS from 7.8 to 24.6 and ITBI, from 1.2 to 4.3; In medium-sized cities, IPTU went from 1.6 to 3.6, ISS from 1.2 to 4.5 and ITBI from 0.2 to 1.0; in small cities, IPTU went from 1.5 to 3.5, ISS from 1.2 to 4.6 and ITBI from 0.4 to 1.1; and in Small cities I, the IPTU went from 0.8 to 1.9, ISS from 0.8 to 3.4, and ITBI from 0.4 to 1.1.

Graph 7 – Municipal revenue in 2003 and 2019 according to the type of tax and size of the municipalities in billions of R$

Source: Prepared by the authors based on data from Santos, Motta and Faria (2020).

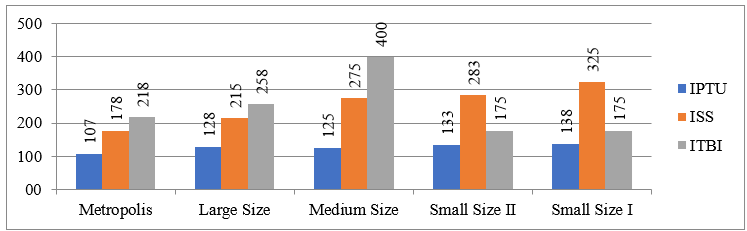

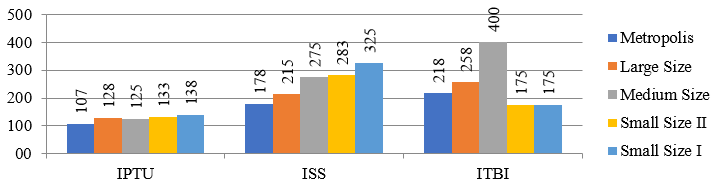

The growth, as shown in Graph 8, occurred in all groups. In the metropolises, it was 107% for IPTU, 177.5% for ISS, and 217.6% for ITBI; in the large cities, 128% for IPTU, 215.4% for ISS, and 258.3% for ITBI; In those of medium size, 125% for IPTU, 275% for ISS and 400% for ITBI; in those of small size II, 133.3% for IPTU, 283.3% for ISS and 175% for ITBI; and in those of small size I, 137.5% for IPTU, 325% for ISS and 175% for ITBI.

Graph 8 – Percentage increase in municipal tax collection between 2003 and 2019 by the size of the municipality and type of tax.

Source: Elaborated by the authors based on data from Santos, Motta, and Faria (2020).

It is noted that small municipalities were the ones that most increased the collection of property tax (IPTU) and service tax (ISS); while metropolitan, large and medium-sized municipalities were the ones that most increased the collection of property tax (ITBI). The growth in taxes among the groups, as shown in Graph 9, for IPTU, varied from 107% to 137.5%; for ISS, from 177.5% to 325%; and for ITBI, from 175% to 400%.

Graph 9 – Percentage increase in municipal tax collection between 2003 and 2009 per type of tax and according to the size of the municipalities

Source: Formulated by the authors based on data from Santos, Motta, and Faria (2020).

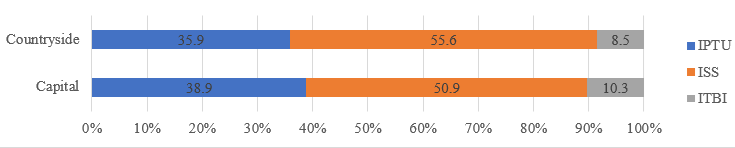

Among the municipalities comprising the groups of metropolises and large cities, the 27 state capitals account for a little more than half (51%) of the municipal collection at the national level. Comparing these with the inland municipalities, as shown in Graph 10, the largest share is from ISS (55.6% and 50.9%), while IPTU is 35.9% and 38.9%, and ITBI is 8.5% and 10.3%.

Graph 10 – Percentage of municipal collection by type of tax according to the category of municipalities (2019)

Source: Formulated by the authors based on data from Santos, Motta, and Faria (2020).

The two groups are similar in the composition of their tax revenues, with each product participating with similar percentages, with a preponderance of taxation on services, followed by the collection of IPTU and ITBI.

Therefore, the municipalities that collect the most taxes are the most populous ones, metropolises and large cities, among them the capitals, and those located in the Southeast and South Regions, reflecting the urban base of the municipal taxes. Among them, the main one is the ISS, which, given its indirect and diffuse collection, meaning that, on service providers in general, has become the primary source in all regions and in all types of municipalities.

This text has traced a current panorama of tax collection of Brazilian municipalities in the fiscal context established by the Federal Constitution of 1988 and the Law of Fiscal Responsibility, according to criteria of grouping municipalities by region, population size and category (capital or interior), making use of the database organized by Santos, Mota, and Faria (2020), which contains information on the three taxes under the jurisdiction of municipalities (IPTU, ISS, ITBI) in the period from 2003 to 2019.

The tax revenues from municipal taxes, according to the competencies established by the Federal Constitution of 1988, should come from the collection of the following taxes: Property and Urban Territory Tax (IPTU); Tax on Transmission of Real Estate (ITBI); Tax on Services of Any Nature (ISS) and totaled, at May 2020 prices, R$ 135,167,685,832.19 in 2019, and R$ 54,365,623,216.47 in 2003, meaning an average annual growth of 6 pp, or 148.6% accumulated in the period.

This growth reflected the heterogeneity of size, socioeconomic reality, and administrative and political capacity to exercise power to tax, being those of the Southeast region and the most populous, above 100 thousand inhabitants, among them the 27 capitals that recorded the highest collection. Although the capitals are approximately 0.5% of the total, they accounted for almost half (48.5%) of the collection of the segment.

This result is an outcome of the municipal tax base based on taxes related to the urban environment, especially on services, as evidenced by the percentage of ISS in the total collection, followed by IPTU, in all groupings (region, population size, and category - capital or inland). However, it is worth noting that the most significant growth occurred in ITBI in the largest municipalities (metropolitan, large, and medium-sized), and in ISS in the group of the small ones. In any case, what can be seen is that large and small municipalities have exercised their tax competencies, collecting the taxes that the Constitution determined.

Therefore, tax collection in Brazilian municipalities more than doubled in the period from 2003 to 2019, having increased the participation of the North, Northeast, and Center-West regions, maintained the percentage in the South Region, and reduced in the Southeast. This, however, did not change the distribution of collection among the regions, with the Southeast remaining with more than three-fifths of the total, which reflects not only its larger population and contribution to the composition of the national GDP, but also its urbanization given the tax base having a seat on the urban environment or activities inherent to it, preferably that one, the ISS, whose collection represents lower administrative and political costs.

AFONSO, J. R. R. Descentralização fiscal, políticas sociais e transferência de renda no Brasil. Gestión Pública. Santiago do Chile, n. 63, p. 1-40, fev., 2007. Disponível em: https://www.cepal.org/sites/default/files/publication/files/7319/S2007604_pt.pdf. Acesso em: 08 abr. 2021.

AFONSO, J. R.R. Federalismo Fiscal Brasileiro: uma visão atualizada. Caderno Virtual (Instituto Brasiliense de Direito Público), Brasília, v. 1, p. 23-47, 2016. Disponível em: https://www.portaldeperiodicos.idp.edu.br/cadernovirtual/article/view/2727/1297. Acesso em: 25 set. 2021.

AFONSO, J. R. R.; ARAÚJO, E. A. A capacidade de gastos dos municípios brasileiros: arrecadação própria e receita disponível. Cadernos de Finanças Públicas, Brasília, a. 1, n. 1, p. 19-30, dez. 2000.

AFONSO, J. R. R.; ARAÚJO, E. A.; NÓBREGA, Marcos Antônio Rios da. O IPTU no Brasil: um diagnóstico abrangente. Rio de Janeiro: FGV, 2013. 79p. (FGV Projetos/ IDP; v. 4). Disponível em: https://fgvprojetos.fgv.br/publicacao/iptu-no-brasil-um-diagnostico-abrangente. Acesso em: 25 set. 2021.

AFONSO, J. R.R.; CASTRO, K. Arrecadação tributária brasileira: uma avaliação atualizada. Cadernos FGV Projetos, Rio de Janeiro: FGV, a. 13, n. 34, p. 65-79, 2018. Disponível em: https://joserobertoafonso.com.br/arrecadacao-tributaria-brasileira-afonso-castro/. Acesso em: 25 set. 2021.

AFONSO, J. R. R.; CASTRO, K . Carga tributaria brasileña en perspectiva histórica: estadísticas revisitadas. Revista de Administração Tributária, Cidade do Panamá, n. 45, p. 139-154, 2019. Disponível em: https://www.hacienda.go.cr/Sidovih/uploads//Archivos/Articulo/Revista%20de%20Administraci%C3%B3n%20tributaria%20N%C2%B045.pdf. Acesso em: 25 set. 2021.

AFONSO, J. R. R.; CORREIA, C. A.; ARAÚJO, E. A.; RAMUNDO, J. C. M.; DAVID, M. D.; SANTOS, R. M. Municípios, Administração e Arrecadação tributária: quebrando tabus. Revista do BNDES, Rio de Janeiro, v. 5, n. 10, p. 3-36, dez, 1998. Disponível em: https://web.bndes.gov.br/bib/jspui/bitstream/1408/11521/2/RB%2010%20Munic%C3%ADpios%2C%20arrecada%C3%A7%C3%A3o%20e%20administra%C3%A7%C3%A3o%20tribut%C3%A1ria%20-%20quebrando%20tabus_P_BD.pdf. Acesso em: 26 out. 2021.

ALEXANDRE, R. Direito Tributário esquematizado. 10. ed., ed. rev., atual. e ampl. São Paulo: Método, 2016.

BRASIL. Decreto Lei nº 406, de 31 de dezembro de 1968. Estabelece normas gerais de direito financeiro, aplicáveis aos impostos sobre operações relativas à circulação de mercadorias e sobre serviços de qualquer natureza, e dá outras providências. Diário Oficial da União: seção 1, Brasília, DF, p. 1131, 31 dez. 1968. Disponível em: https://www2.camara.leg.br/legin/fed/declei/1960-1969/decreto-lei-406-31-dezembro-1968-376809-publicacaooriginal-1-pe.html. Acesso em: 26 jul. 2021.

BRASIL. [Constituição (1988)]. Constituição da República Federativa do Brasil de 1988. Brasília, DF: Presidência da República, 1988. Disponível em: http://www.planalto.gov.br/ccivil_03/Constituicao/. Constituiçao.htm. Acesso em: 16 fev. 2021.

BRASIL. Lei Complementar, nº. 101, de 4 maio 2000. LRF – Lei

de Responsabilidade Fiscal. Estabelece normas de finanças públicas voltadas para a responsabilidade na gestão fiscal e dá outras providências. Diário Oficial da União: seção 1, Brasília, DF, ano CXXXVIII, n. 86, p. 1-9, 05 maio 2000. Disponível em: https://pesquisa.in.gov.br/imprensa/jsp/visualiza/index.jsp?data=05/05/2000&jornal=1&pagina=82&totalArquivos=152. Acesso em 23 fev. 2023.

BRASIL. Lei Complementar nº 116, de 31 de julho de 2003. Dispõe sobre o Imposto Sobre Serviços de Qualquer Natureza, de competência dos Municípios e do Distrito Federal, e dá outras providências. Diário Oficial da União: seção 1, Brasília, DF, ano CXL, n. 147, p. 3-6, 01 ago. 2003. Disponível em: https://pesquisa.in.gov.br/imprensa/jsp/visualiza/index.jsp?jornal=1&pagina=3&data=01/08/2003. Acesso em: 17 jul. 2021.

BRASIL. Ministério de Estado das Cidades. Portaria MCid nº 511, de 07 de dezembro de 2009. Dispõe sobre Diretrizes para a criação, instituição e atualização do Cadastro Territorial Multifinalitário (CTM) nos municípios brasileiros. Diário Oficial da União: seção 1, Brasília, DF, nº 234, p. 75. 8 dez. 2009. Disponível em: https://pesquisa.in.gov.br/imprensa/jsp/visualiza/index.jsp?jornal=1&pagina=75&data=08/12/2009. Acesso em: 26 jul. 2021.

BRASIL. Lei Complementar nº 157, de 29 de dezembro de 2016. Altera a Lei Complementar no 116, de 31 de julho de 2003, que dispõe sobre o Imposto Sobre Serviços de Qualquer Natureza, a Lei no 8.429, de 2 de junho de 1992 (Lei de Improbidade Administrativa), e a Lei Complementar no 63, de 11 de janeiro de 1990, que dispõe sobre critérios e prazos de crédito das parcelas do produto da arrecadação de impostos de competência dos Estados e de transferências por estes recebidos, pertencentes aos Municípios, e dá outras providências. Diário Oficial da União: seção 1, Brasília, DF, ano CLIV, n. 104, p. 1, 01 jun. 2017a. Disponível em: https://pesquisa.in.gov.br/imprensa/jsp/visualiza/index.jsp?data=01/06/2017&jornal=1&pagina=1&totalArquivos=256. Acesso em: 26 jul. 2021.

BRASIL. Código tributário nacional. 3. ed. Brasília: Senado Federal, Coordenação de Edições Técnicas, 2017b. 69 p. Disponível em: https://www2.senado.leg.br/bdsf/bitstream/handle/id/531492/codigo_tributario_nacional_3ed.pdf. Acesso em: 17 jul. 2021.

BRASIL. Congresso Nacional. Estudo e consulta: Reforma Tributária: PEC 110/2019, do Senado Federal, e PEC 45/2019, da Câmara dos Deputados. Brasília, DF: Consultoria Legislativa, 2019a. Disponível em: https://bit.ly/3dcS0p5. Acesso em: 12 mar. 2020.

BRASIL. Senado Federal. Proposta de Emenda à Constituição nº 188, de 2019. PEC do Pacto Federativo. Altera arts. 6º, 18, 20, 29-A, 37, 39, 48, 62, 68, 71, 74, 84, 163, 165, 166, 167, 168, 169, 184, 198, 208, 212, 213 e 239 da Constituição Federal e os arts. 35, 107,109 e 111do Ato das Disposições Constitucionais Transitórias; acrescenta à Constituição Federal os arts. 135-A, 163-A, 164-A, 167-A, 167-B, 168-A e 245-A; acrescenta ao Ato das Disposições Constitucionais Transitórias os arts. 91-A, 115, 116 e 117; revoga dispositivos constitucionais e legais e dá outras providências. Brasília, DF: Senado Federal, 2019b. Disponível em: https://www25.senado.leg.br/web/atividade/materias/-/materia/139704. Acesso em: 17 jun. 2021.

BREMAEKER, F. E. J. de. Mitos sobre as finanças dos municípios brasileiros. Revista de Administração Municipal, Rio de Janeiro, v. 41, n. 212, p. 6-21, jul./set., 1994. Disponível em: http://lam.ibam.org.br/revista_detalhe.asp?idr=104. Acesso em: 20 jul. 2021.

FERNANDES, L. H. dos S. Eficiência tributária municipal e seus determinantes: uma abordagem semi-paramétrica via regressão beta. 2017. 69f. Dissertação (Mestrado em Economia do Setor Público) – Programa de Pós-Graduação do Departamento de Economia da Universidade Federal da Paraíba, João Pessoa, 2017. Disponível em: https://repositorio.ufpb.br/jspui/bitstream/123456789/12514/1/Arquivototal.pdf. Acesso em: 26 jul. 2021.

HAMILTON, A.; MADISON, J.; JAY, J. The Federalist Papers. Tradução: Maria Luiza X. de A. Borges. Edição integral. Rio de Janeiro: Nova Fronteira, 1993.

HARADA, K. ISS: doutrina e prática. 2. ed., ed. reform., rev. e ampl. São Paulo: Atlas, 2014.

IBGE – Instituto Brasileiro de Geografia e Estatística. IBGE divulga as Contas Regionais 2003 – 2006. Agência IBGE notícias, 14 nov. 2008. Disponível em: https://agenciadenoticias.ibge.gov.br/agencia-sala-de-imprensa/2013-agencia-de-noticias/releases/13571-asi-ibge-divulga-as-contas-regionais-2003-2006. Acesso em: 07 set. 2021.

IBGE – Instituto Brasileiro de Geografia e Estatística. Coordenação de Contas Nacionais, Coordenação de Geografia, Coordenação de Recursos Naturais e Estudos Ambientais. Produto interno bruto dos municípios: 2018: PIB dos Municípios [informativo]. Rio de Janeiro: IBGE, 2020. 16 p. (Contas Nacionais, n. 78). Disponível em: https://biblioteca.ibge.gov.br/visualizacao/livros/liv101776_informativo.pdf. Acesso em: 17 jul. 2021.

MASSARDI, W. de O.; ABRANTES, L. A. Esforço fiscal, dependência do FPM e desenvolvimento socioeconômico: um estudo aplicado aos municípios de Minas Gerais. Revista de Gestão, São Paulo, v. 22, n. 3, p. 295-313, 2015.

ORAIR, R. A.; ALENCAR, A. A. Esforço Fiscal dos Municípios: indicadores de condicionalidade para o sistema de transferências intergovernamentais. Brasília: Esaf, 2010. Monografia premiada com o primeiro lugar no XIII Prêmio Tesouro Nacional. Tópicos Especiais de Finanças Públicas. Brasília-DF. Disponível em: https://premios.tesouro.gov.br/stn2010/assets/pdf/tema4/Tema%204%20-%201%20lugar%20-%20Rodrigo%20Orair%20e%20Andre%20Alencar.pdf. Acesso em: 17 jul. 2021.

SANTOS, C. H. M dos; MOTTA, A. C. S. V.; FARIA, M. E. de. Estimativas anuais da arrecadação tributária e das receitas totais dos municípios brasileiros entre 2003 e 2019. Carta de Conjuntura do Ipea, Brasília, n. 48, julho de 2020. Disponível em: https://www.ipea.gov.br/cartadeconjuntura/index.php/2020/07/estimativas-anuais-da-arrecadacao-tributaria-e-das-receitas-totais-dos-municipios-brasileiros-entre-2003-e-2019/. Acesso em: 18 mar. 2021.

SERRA, J.; AFONSO, J. R. R. Federalismo Fiscal à Brasileira: algumas reflexões. Revista do BNDES, Rio de Janeiro, v. 6, n. 12, p. 3-30, 1999. Disponível em: https://www.bndes.gov.br/SiteBNDES/export/sites/default/bndes_pt/Galerias/Arquivos/conhecimento/revista/rev1201.pdf. Acesso em: 20 mar. 2020.

SIQUEIRA, K. J. da S. P. de; PAES, N. L.; LIMA, R. C. de A. Eficiência na administração tributária dos municípios: o caso da arrecadação em Pernambuco. Revista Brasileira de Economia de Empresas, Brasília, v. 16, n. 2, p. 97-120, [s.d.], 2016.

SUZART, J. A. da S.; ZUCCOLOTTO, R.; ROCHA, D. G. da. Federalismo fiscal e as transferências intergovernamentais: um estudo exploratório com os municípios brasileiros. Advances in Scientific and Applied Accounting, São Paulo, v.11, n.1, p. 127-145, jan./abr. de 2018.

TRISTÃO, J. A. M. A administração tributária dos municípios brasileiros: uma avaliação do desempenho da arrecadação. 2003. 172 p. Tese (Doutorado em Administração) – Programa de Pós-Graduação da Escola de Administração de Empresas de São Paulo, da Fundação Getúlio Vargas, São Paulo, 2003.

WEBER, M. A “objetividade” do conhecimento das ciências sociais. Tradução de Gabriel Cohn. São Paulo: Ática, 2006.