Abstract

Studies show that, currently, sustainability is one of the strategies used by many organizations to carry out their activities. To meet their goals, organizations need tools that disseminate their sustainable actions. In this context, the sustainability report is an important tool that indicates the social, economic and environmental factors of organizations, with greater transparency. Considering the main communication instrument on sustainable performance, the guidelines of the Global Reporting Initiative (GRI) allow organizations to outsource their actions in the environmental, social, and economic dimensions. The objective of this work is to examine sustainability reports of large Brazilian companies in order to verify the institutional profile according to the global reporting initiative (GRI) standard and, based on the respective parameters, perform critical analysis of sustainable practices. The research is characterized as qualitative, exploratory, documentary and cross-sectional. The results of the research indicate that, among the institutionalized sustainable objectives, many have been achieved. However, it is perceived that there are still challenges to be faced by organizations, especially with regard to the environmental dimension, which constitutes the basis of social and economic relations.

Keywords: Sustainability, Sustainable Development, Large Enterprises, Sustainability Reports, Indicators, GRI.

Resumo

Estudos mostram que, atualmente, a sustentabilidade é uma das estratégias utilizadas por muitas organizações para efetivar a atividade fim. Para atender seus objetivos, as organizações precisam de instrumentos que divulguem suas ações sustentáveis. Nesse contexto, o relatório de sustentabilidade é uma importante ferramenta que indica os fatores sociais, econômicos e ambientais das organizações, com maior transparência. Considerado o principal instrumento de comunicação sobre desempenho sustentável, as diretrizes da Global Reporting Initiative (GRI) permitem às organizações externalizar suas ações nas dimensões ambiental, social e econômica. O objetivo deste trabalho é examinar relatórios de sustentabilidade de grandes empresas brasileiras a fim de verificar o perfil institucional segundo o padrão da Global Reporting Initiative (GRI) e, a partir dos respectivos parâmetros, realizar análise crítica das práticas sustentáveis. A pesquisa caracteriza-se como qualitativa, exploratória, documental e transversal. Os resultados da pesquisa apontam que, dentre os objetivos sustentáveis institucionalizados, muitos têm sido alcançados. No entanto, percebe-se que ainda há desafios a serem enfrentados pelas organizações, especialmente no que tange a dimensão ambiental, que constitui a base das relações sociais e econômicas.

Palavras-chave: Sustentabilidade, Desenvolvimento Sustentável, Grandes Empresas, Relatórios de Sustentabilidade, Indicadores, GRI.

Sustainable development, according to the needs of society, requires constant and new priorities, which can be effected only with behavioral ethics, social and collective interests, which encompass key changes in the structure of production and consumption, enabling inversions in the framework of environmental degradation and social misery from its causes (NEVES, 2019).

Sustainable activity is one that can be maintained for indeterminate periods, so as not to be exhausted, despite the unforeseen events that may occur. The concept of sustainability, in a context applied in a sustainable society, does not put at risk natural resources such as air, water, soil and plant and animal life on which society depends. Sustainable development improves the quality of life of human beings and the ecosystem, respects their reproductive, production and development capacities. Ecological sustainability enables efficient use of potential resources in the various ecosystems, in addition to reducing irresponsible consumption and reducing pollution (SOUZA, 2018).

The concern to practice sustainable development implies and consequently expands the way organizations operate, involving, in addition to purely economic considerations, environmental and social preoccupations (FONSECA et al., 2011). It is an awareness that has been increased since the second half of the 20th century, from the publication of reports and the convening of international meetings to popularize the theme and create action plans capable of responding to the challenges posed by climate emergencies and socioeconomic disparities.

The preparation of sustainability reports has been an important practice in the evaluation and dissemination of sustainability in organizations (BRADFORD; EARP; WILLIAMS, 2014). According to the Ethos Institute of Social Responsibility (INSTITUTO ETHOS, 2014), sustainability reports can be defined as annual statements of projects, benefits and social actions directed to all stakeholders – whether employees, investors, governments, market, shareholders, and the community – whose function is to make public the responsibilities, and the concerns of companies about the value of people and life on the planet, thus providing links between everyone in society.

The non-governmental organization Global Reporting Initiative (GRI) has developed a document structure based on a series of guidelines that has become a reference for the preparation of sustainability reports, including the membership of business organizations from various countries (MARIMON et al., 2012).

In this context, the following question summarizes the goal of this research, to be investigated: What is the sustainable profile of large Brazilian companies, according to the criteria of the Global Reporting Initiative?

This work aims to examine sustainability reports of large Brazilian companies in order to verify the institutional profile according to the global reporting initiative (GRI) standard and based on the respective parameters perform critical analysis on sustainable practices.

The ideals of sustainable developments permeate together with other demands of society, such as the need for new forms and ways of relationship with the environment, aiming both the conservation of its essential characteristics and the development of all forms of life. According to Lozano (2008, p. 1838) "the concepts of sustainable development and sustainability have emerged as alternatives to help understand, combat and reduce economic disparities, environmental degradation and current and potentially future social diseases."

Several studies, such as those of Lozano (2008), Rogers, Kazi and Boyd (2008) and Van Bellen (2008) indicate that the conceptions of sustainable development involve differentiated perspectives and, consequently, generate different interpretations.

The classic concept of sustainable development emerged in the 1970s through studies by the International Union for Conservation of Nature. The World Conservation Strategy Report, from 1980, considers that the social and ecological dimensions are important sustainable aspects, as well as the respective economic factors, living and non-living resources, which provide advantages of alternative actions in the short, medium, and long term. The focus of the concept is environmental integrity.

In 1973 Maurice Strong coined the term Ecodevelopment, based on principles formulated by Ignacy Sachs. Ecodevelopment sought to improve the concept of development, in a positive sum with nature, based on social justice, economic efficiency and ecological prudence (NASCIMENTO; WE READ; MELLO, 2008).

In 1987, through the Brundtland Report, the concept of sustainable development was disseminated worldwide. The Report was developed by the UN World Commission on Environment and Development. From Brundtland's conception, the emphasis becomes on the human element, emphasizing the need for a balance between the environmental, economic, and social dimensions (VAN BELLEN, 2008), in view of concerns for future generations. The concept expanded the scope of the environmental dimension, adding economic and social issues as pillars of a tripod (ELKINGTON, 2012).

Elkington (2012) writes that the UN World Commission included in the main objectives of the Brundtland Report concepts of economic growth reactivation processes. However, it did it in a new way: meeting the vital needs of the human being, such as food, water supply, energy, and jobs, increase and conservation of natural resources, new directions to technology and risk management, incorporation of environmental issues into decision-making.

Van Bellen (2008) states that the Brundtland report's proposal is the most widely adopted globally, with a view to its direct influence on the public policies of the World Bank and international bodies such as the United Nations Environment Programme (UNEP), and the International Union for Conservation of Nature (IUCN), the World Union for Nature, international development agencies, research and promotion organizations, activist groups, among others.

According to Rogers, Peter and Boyd (2008), sustainable development is a dynamic process of change in which resource exploration, investment direction, technological development orientation and institutional change are consistent with present and future needs.

Lozano (2008) classifies the concept of sustainable development in five perspectives, such as: (i) the ones from conventional economists (ii) non-environmental degradation (iii) the integrator of environmental, social, and economic aspects (iv) intergenerational, and (v) holistic. For the author, the best perspective is holistic, considering that it results from the union between the integrative and intergenerational perspectives. While the integrative perspective contemplates essential aspects for development (environment, economy and society) in the short and long term, the intergenerational perspective extends the temporality to a longitudinal level. Thus, the holistic perspective becomes more comprehensive and more appropriate to the current reality. The author's view does not mischaracterize the tripod of sustainability, it only adds an important component to the tripod (Triple Bottom Line).

Sachs (2002), Polish economist and central author for the subject, attributes to sustainable development, eight dimensions: social, cultural, ecological, environmental, territorial, economic, national politics and international politics.

It is verified, therefore, that sustainable development is a phenomenon that reaches different dimensions or perspectives. Each of them contributes to the conceptual understanding of the phenomenon and the implementation of practices that can ensure the inhabitants of Planet Earth a livable and more promising future.

In any of the dimensions studied, it can be understood that sustainability is a harmonious coexistence between humanity and nature. To be sustainable is to live responsibly on the Planet, in such a way that it is possible to withstand the impacts that human beings cause throughout life. Sustainability is preserving it for future generations. It is society's expectation of people, governments and organizations (PAZ; KIPPER, 2016).

Elkington (2012) argues that, in an organizational context, sustainability is the balance between three pillars, namely a Triple Bottom Line: environmental, social, and economic. For the author, sustainable development is the goal to be achieved and sustainability is the process to achieve it.

The environmental dimension acquires extreme importance in a sustainability report, since it allows measuring the impacts of human and organizational activities on the environment. Van Bellen (2008) and Elkington (2012) believe that the environmental dimension is intrinsic to the natural capital. It is the defense of a concept that sees, from the perspective of production costs, important values in natural resources in relation to a product or service, treating them as capital, in the same way as economic resources are treated.

In this context, an organization that depends on nature for its success should consider natural goods as part of its capital. This is because a possible shortage of natural resources directly affects the productivity and financial health of the business, resulting in undesirable consequences.

Studies show that in sustainability there are more discussions about the economic and environmental dimensions and less about the social dimension (SARKIS; HELMS; HERVANI, 2010; VIFELL, VIFELL, SONERYD, 2012). However, the social dimension is fundamental, considering being a dimension that leads the organization to consider the human being as a key element (LOURENÇO; OAK, 2013). From this perspective, one of the objectives of an organization should be to ensure that people have equal conditions of access to goods, good quality services for a dignified life, guiding their development through substantive freedoms and generation of opportunities (SEN, 2010). This makes the human being, within or around organizations, be considered as a significant component in the debates involving the search for sustainable development.

The economic dimension also has great importance in addressing sustainability in organizations. Elkington (2012) argues that sustainable development is only possible, in the economic dimension, when quality of life has a preponderance over the concern with the amount of production. Also, according to Van Bellen (2008), the crisis arises when the economy, or economic subsystem, grows in such a way that the demand on the environment exceeds its limits. It is a situation that has been increasingly under the pressures exerted by economic growth.

Castro, Campos and Trevisan (2018) take a critical look at organizational sustainability, citing examples of companies that, despite having extensive knowledge of the principles of sustainability, allow other interests to prevail, such as the accumulation of capital and the expansion of political and economic power.

According to Silva (2021), the practice known as greenwashing, adopted by companies that "paint green" their products and their institutional image to make them look sustainable, seems to compromise the possibility of the operation of effectively sustainable organizations.

Nevertheless, there are organizations that effectively invest in a sustainable and socially responsible culture, driven by real commitment to social and environmental agendas, going beyond simple, purely superficial marketing (ABRAMOVAY, 2012). There are companies that "are responsible because they believe they should be responsible, not because others demand them to be" (BARAIBAR-DIEZ; SOTORRIO, 2018, p. 15).

Amid the multiple pressures arising from increased social perception about the need for sustainable actions and also distrust of advertisements and the practice of greenwashing, organizations have increasingly bet on the publication of sustainability reports (SILVA, 2021). It is an annual document voluntarily produced by the company after "internal audit" to map the degree of sustainability of the company and its impacts on society and the planet. This "audit" seeks to understand management, actions and evaluate them according to environmental, social, economic and even governance criteria (INSTITUTO ETHOS, 2014).

In addition, in order to be a guiding platform for changes of ideas and ideals, it is an important and advantageous operational tool, enabling the establishing objectives and goals, operational transformations, control of externalities, communication of positive and negative impacts, and gathering information that can influence the organization's policy, strategy and operations.

Feil, Strasburg and Naime (2013) argue that sustainability reports are annual statements of projects, benefits and social actions directed at all stakeholders, i.e., employees, investors, governments, the market, shareholders and the community, whose function is to make public the responsibility and concern of the company in relation to people and life on Earth, creating links with society. Thus, sustainability reports are the main communication tool of the social, economic and environmental performance of corporate organizations.

Preparing sustainability reports to measure and disseminate social and environmental impacts caused by the daily activities of organizations has been a practice incorporated by companies from several countries. The adhering to the values that enable reports consistent with the principles of sustainability has been voluntary and aims to: (i) support and facilitate the management of corporate sustainability issues in a systematic manner, (ii) disclose risks and opportunities, (iii) and build a more transparent corporate reputation. The information in the reports can also serve the growing demands of society and, mainly, as a response to the demands of stakeholders for companies to explain their socio-environmental responsibility actions, their actions in the environment in which they are inserted (CAMPOS et al., 2013).

In order to be able to produce their own sustainability report, organizations need to carry out some actions, such as: (i) making the decision to produce the report, through an internal articulation, (ii) organize the information, reporting its strategic, deliberate and emerging actions in documents, as mentioned above, (iii) train people to become able to organize information and produce the report, (iv) raise awareness and mobilize its internal and external audiences to engage in sustainable actions, (v) make your sustainability report a public document through the institutional website and social networks, (vi) adopt strategies so that sustainable actions are inserted and practiced more and more, becoming part of the culture in the organization, and (vii) set annual sustainable targets so that, each year, the sustainability report is expanded and improved (CAMPOS et al. , 2013).

The preparation of its own sustainability report allows organizations to: (i) demonstrate their commitment to economic, social and environmental aspects, (ii) plan its activities, becoming more sustainable every day, (iii) demonstrate organization in the various segments that involve its activities, (iv) demonstrate that sustainable actions do not only go up to theoretical discussions, on the contrary, it also involves practical actions that help solve the problems faced by human beings, (v) create a culture of sustainable actions both within the internal environment and in the community around them, (vi) to achieve transparency in relations with the community and society, (vii) to present capacity for participation and influence, both in the community and its surroundings and in the broad society, (viii) show willingness to comply with applicable legislation (CAMPOS et al. , 2013).

These sustainable activities provide important positive values for organizations, increase the chances of loyalty with the market and also enable periodic analysis of data for performance comparison with other organizations.

Therefore, publishing a sustainability report is very important. However, the choice of which orientation to use or consult will also influence the results obtained through the analysis of factors and the economic, social and environmental dimensions, enabling the organization and its respective development to be increasingly sustainable.

There is a considerable list of organizations that have developed sustainability reports. In this context, the Global Reporting Initiative (GRI), created in 1997 by the U.S. NGO Coalition for Environmentally Responsible Economics – CERES, in Boston, USA stands out. It is composed of a multistakeholder network (diversified network in public interest), whose mission is to develop and disseminate globally guidelines for the structuring of sustainability reports around the world (SOUZA, 2018).

The first version of the Guidelines for sustainability reports, according to the GRI model, was launched in 2000, with the participation of volunteers from the business sector, NGOs, labor organizations, institutional investors, human rights activists, audit and consulting firms, UN agencies, among others. The second generation of guidelines, known as G2, was launched in 2002 at the World Summit on Sustainable Development in Johannesburg – South Africa. At that time, the United Nations Environment Programme (UNEP) embraced GRI and invited UN member states to host it. The Netherlands was chosen to be the host country (GRI, 2013).

After updates and improvements, in 2013 came the latest version of GRI, G4, which, unlike previous guidelines, suggests profound changes in the effectiveness of sustainability in companies.

The structure proposed by GRI (2013) has four elements that direct the preparation of an effective sustainability report, as shown in Table 1.

Table 1 - GRI guidelines for sustainability reporting

|

GUIDELINE |

DESCRIPTION |

|

Guidelines for the preparation of sustainability report |

Principles for defining the content of the report and ensuring the quality of the information reported. They also include the content of the report, performance indicators and other disclosure items, as well as guidance on the preparation of the sustainability report. Gri guidelines are developed with the participation of international working groups, stakeholders and public consultation. |

|

Indicator protocols |

Provide definitions, build guidance, and other information to ensure consistency of performance indicators. |

|

Sector supplements |

They are publications with interpretations and guidance on the application, of indicators, in specific sectors. |

|

Technical protocols |

They guide the preparation of the sustainability report including the establishment of limits. |

Source: Elaborated by the authors, based on GRI version G4 (2013).

Through these four structuring elements, an important sustainability report can be drawn up. According to GRI, the report should present in its structure: the profile of the organization, in which information is reported to understand organizational performance, including its strategy, profile and governance, information on the form of management, with data that explains the context in which the organization's performance should be interpreted, and performance indicators, to demonstrate economic, environmental, and social performance. The social dimension is subdivided into the categories: labor practices, human rights, society and product responsibility (GRI, 2013).

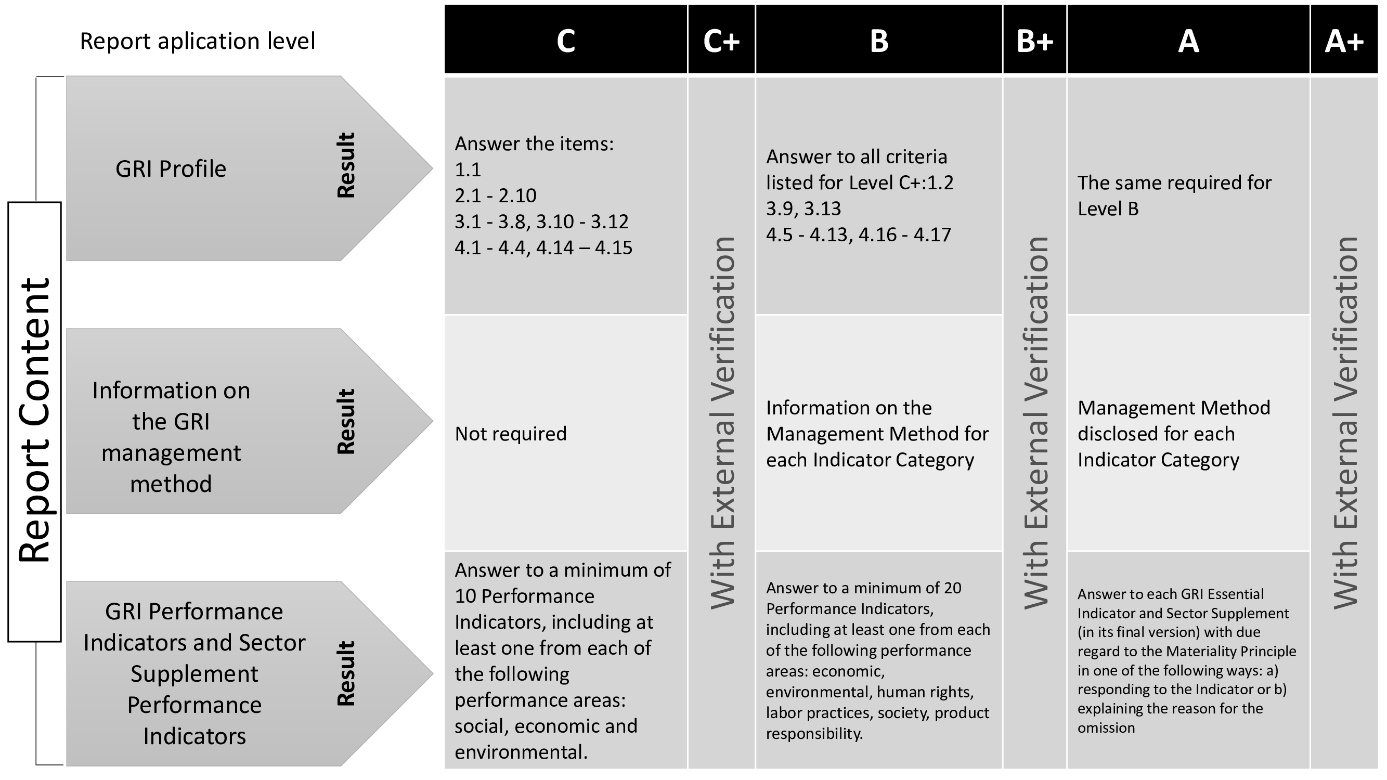

To prepare the sustainability report, the organization can opt for one of the three levels proposed by GRI. Each level regulates items of the organization's profile according to guidelines, sector supplements, if any, as well as the number of performance indicators (GRI, 2013).

According to GRI (2013), application levels can be classified at level C (beginner), B (intermediate) and A (advanced). The organization may also self-declare an over-the-top (+) point at each level (e.g., C+, B+, A+). In this case, after the creation of the sustainability report, there will be an external audit in the organization, for the certification. Level "C", for example, establishes a minimum of ten performance indicators that must be answered, while level B requires a minimum of twenty indicators. Level A, considered complete, requires the completion of all performance indicators. Figure 1 presents the application levels, in a summarized way, with their respective requirements.

Figure 1 - GRI application levels

Source: GRI Primer (2013, s. p.).

The performance indicators of the G4 version are divided into three dimensions: 34 environmental, 09 economic and 47 social, totaling 91 indicators.

GRI has guidelines that can be used by any and all organizations, regardless of its economic sector. In Brazil, within the scope of the private sector, important companies already produce sustainability reports based on guidelines proposed by GRI. According to GRI (2013), among the reasons for organizations to release a sustainability report are: (i) understanding the risks and opportunities they face, (ii) improvement of reputation and brand loyalty, (iii) understanding of stakeholders about performance and impacts of sustainability, (iv) emphasis on the relationship between financial and non-financial organizational performance, (v) influence on strategy, long-term management policy and business plans, (vi) benchmarking and evaluation of the effectiveness of laws, standards, codes, performance parameters and voluntary initiatives, (vii) demonstration of how the organization influences and is influenced by expectations of sustainable development, (viii) comparison of internal organizational performance with the performance of other organizations, (ix) compliance with applied national standards, with stock exchange requirements.

The nature of this research is basic, considering that it does not present immediate purposes and does not produce knowledge to be used in other researches.

Regarding the approach to the problem, the research is characterized as qualitative. Navarrete (2004) explains that the qualitative search has as its initial point the understanding of the intention of the social act, that is, the structure of motivations that the subjects have, the purpose that guides their conduct, the values, feelings, beliefs that direct it to a determined purpose. Thus, qualitative analysis favors the understanding of factors related to decisions that, in turn, attribute meaning to the information used in the management process.

As for the objectives, this is an exploratory research, which allows making the problem explicit or constructing hypotheses (RICHARDSON, 2017). According to Gil (2019), an exploratory study is adopted in situations where the research object is little known or has been little studied. Thus, the exploratory study provides greater familiarity with the problem, allowing to explain it better.

Regarding the procedures for data collection, the research was characterized as documentary. According to Gil (2019), documentary research is an important technique in qualitative research, either complementing information obtained by other techniques, or unlooking new aspects of a theme or problem. Documentary research uses primary sources, that is, data and information that have not yet been treated scientificly or analially.

The sampling of this research is non-probabilistic and intentional, taking into account the accessibility of the researcher to the data, as instructed by Richardson (2017) and involved the analysis of sustainability reports published by the ten largest Brazilian companies that fall under the GRI model. The companies (which fall under the GRI model) were identified based on the list of the largest companies in Brazil according to the ranking published by portal Estadão (2019).

Regarding the dimension of time, the research is characterized as cross-sectional, considering that the study was conducted only once and reveals the situation of a given moment (COOPER; SCHINDLER, 2016). It portrays, therefore, the sustainability stage of the respective companies only in the year in which it was analyzed: 2019.

Content analysis was chosen as a technique for analyzing the collected data. In recent years, content analysis has been highlighted among qualitative methods, and, therefore, has gained legitimacy. The importance of content analysis for organizational studies has been increasing, having evolved due to the concern with scientific rigor and depth of research (MOZZATO; GRZYBOVSKI, 2011). As recommended by Bardin (2016, p. 121), the study pursued the following phases of content analysis: (i) pre-analysis, (ii) exploitation of the material, and (iii) treatment of the results, which involves inference and interpretation.

In this topic, the results of the research are presented and analyzed. To facilitate understanding, three categories of analysis were created: environmental dimension, social dimension, and economic dimension. In each dimension, we tried to identify the practices adopted by the companies, in line with or dissonance with the GRI booklet, G4 version of 2013.

Table 2 presents GRI G4 environmental aspects and their respective indicators.

Table 2 - Environmental aspects and respective indicators of the GRI G4 2013 version.

|

Environmental Aspects |

Environmental Indicators |

Acronyms |

|

Materials |

Reduction in the use of materials |

EN1 |

|

Use of recycled inputs |

EN2 |

|

|

Energy |

Energy consumption within the organization |

EN3 |

|

Indirect energy consumption (travel, transport, etc.) |

EN4 |

|

|

Improvements made to increase energy efficiency |

EN5 |

|

|

Reduced energy consumption |

EN6 |

|

|

Reduction in indirect energy consumption (travel, transport, etc.) |

EN7 |

|

|

Water |

Total volume of water withdrawn in m3/year in any source |

EN8 |

|

Water sources significantly affected by water withdrawal |

EN9 |

|

|

Volume of recycled and reused water |

EN10 |

|

|

Biodiversity |

Monitoring of activities carried out in protected areas |

EN11 |

|

Impacts of activities on biodiversity in protected areas |

EN12 |

|

|

Prevention or repair of negative impacts associated with activities |

EN13 |

|

|

Protected or restored habitats |

EN14 |

|

|

Environmental impact studies with specific goals and objectives |

EN15 |

|

|

Emissions |

Direct greenhouse gas (GHG) emissions |

EN16 |

|

Direct GHG emissions from energy acquisition |

EN17 |

|

|

Intensity of direct greenhouse gas (GHG) emissions |

EN18 |

|

|

Reduction of direct greenhouse gas (GHG) emissions |

EN19 |

|

|

Emissions of ozone-depleting substances (SDO) |

EN20 |

|

|

Emissions of NOx, SOx and other significant atmospheric emissions |

EN21 |

|

|

Effluents and Waste |

Total disposal of water, its quality and disposal |

EN22 |

|

Total waste generated, types and destination |

EN23 |

|

|

Occurrence of significant leaks |

EN24 |

|

|

Hazardous waste generated, transported, imported, exported |

EN25 |

|

|

Bodies of water, habitats and biodiversity affected by effluents and waste |

EN26 |

|

|

Products and Services |

Mitigation of environmental impacts generated by the organization's activities |

EN27 |

|

Products and packaging recovered in relation to sales volume |

EN28 |

|

|

Compliance |

Fines and penalties received for inflicting environmental legislation |

EN29 |

|

Transport |

Environmental impacts arising from various transport activities |

EN30 |

|

General |

Total investments and spending on environmental protection |

EN31 |

|

Supplier Environmental Assessment |

New suppliers selected based on environmental criteria |

EN32 |

|

Environmental impacts on the supply chain and mitigating measures |

EN33 |

|

|

Complaints Environmental Impacts |

Complaints received regarding environmental impacts and solutions |

EN34 |

Source: Elaborated by the authors based on GRI (2013).

According to the GRI booklet, each indicator indicated in table 2 is followed by an explanatory text, which makes it possible to identify whether or not the company is in line with the GRI proposal. Table 3 presents the results of the environmental dimension in the companies surveyed, as recorded in the sustainability reports. The companies surveyed, according to the Estadão Portal ranking (2019), are, in alphabetical order, the following: BR Distribuidora, Braskem, Bunge, Cargill, Carrefour, Ipiranga, Petrobrás, Raízen, Vale and Vivo. The green colors point out the indicators that are in line with the GRI booklet, version 4, of 2013. The red colors point out the indicators that are not included in the company's report and are therefore in disagreement with the GRI booklet.

Table 3 - Identification of the practices adopted by companies in the environmental dimension, in line with the GRI booklet.

|

Environmental Aspects of GRI G4 |

Acronyms of Indicators |

Identification of Environmental Indicators in Reports |

|||||||||

|

BR Distribuidora |

Braskem |

Bunge |

Cargill |

Carrefour |

Ipiranga |

Petrobrás |

Raízen |

Vale |

Vivo |

||

|

Materials |

EN1 |

|

|

|

|

|

|

|

|

|

|

|

EN2 |

|

|

|

|

|

|

|

|

|

|

|

|

Energy |

EN3 |

|

|

|

|

|

|

|

|

|

|

|

EN4 |

|

|

|

|

|

|

|

|

|

|

|

|

EN5 |

|

|

|

|

|

|

|

|

|

|

|

|

EN6 |

|

|

|

|

|

|

|

|

|

|

|

|

EN7 |

|

|

|

|

|

|

|

|

|

|

|

|

Water |

EN8 |

|

|

|

|

|

|

|

|

|

|

|

EN9 |

|

|

|

|

|

|

|

|

|

|

|

|

EN10 |

|

|

|

|

|

|

|

|

|

|

|

|

Biodiversity |

EN11 |

|

|

|

|

|

|

|

|

|

|

|

EN12 |

|

|

|

|

|

|

|

|

|

|

|

|

EN13 |

|

|

|

|

|

|

|

|

|

|

|

|

EN14 |

|

|

|

|

|

|

|

|

|

|

|

|

EN15 |

|

|

|

|

|

|

|

|

|

|

|

|

Emissions |

EN16 |

|

|

|

|

|

|

|

|

|

|

|

EN17 |

|

|

|

|

|

|

|

|

|

|

|

|

EN18 |

|

|

|

|

|

|

|

|

|

|

|

|

EN19 |

|

|

|

|

|

|

|

|

|

|

|

|

EN20 |

|

|

|

|

|

|

|

|

|

|

|

|

EN21 |

|

|

|

|

|

|

|

|

|

|

|

|

Effluents and Waste |

EN22 |

|

|

|

|

|

|

|

|

|

|

|

EN23 |

|

|

|

|

|

|

|

|

|

|

|

|

EN24 |

|

|

|

|

|

|

|

|

|

|

|

|

EN25 |

|

|

|

|

|

|

|

|

|

|

|

|

EN26 |

|

|

|

|

|

|

|

|

|

|

|

|

Products and Services |

EN27 |

|

|

|

|

|

|

|

|

|

|

|

EN28 |

|

|

|

|

|

|

|

|

|

|

|

|

Compliance |

EN29 |

|

|

|

|

|

|

|

|

|

|

|

Transport |

EN30 |

|

|

|

|

|

|

|

|

|

|

|

General |

EN31 |

|

|

|

|

|

|

|

|

|

|

|

Supplier Environmental Assessment |

EN32 |

|

|

|

|

|

|

|

|

|

|

|

EN33 |

|

|

|

|

|

|

|

|

|

|

|

|

Complaints Environmental Impacts |

EN34 |

|

|

|

|

|

|

|

|

|

|

Source: Elaborated by the authors based on the research data.

Table 3 makes it possible to analyze initiatives related to environmental sustainability based on the indicators, and the challenges involved in this issue. It is noteworthy that the companies that stood out in the environmental area were: Petrobras, Braskem and Carrefour.

The sustainability indicators specific to the context of the best performing company are those identified by the acronyms: EN5, EN16, EN17, EN18, EN29, EN33, EN34. These indicators incorporate issues such as emissions, complaints, environmental impacts and energy.

It is emphasized that the indicators EN13, EN14, EN25, EN26 and EN30 did not obtain relevant results, which evidences the lack of actions directed to biodiversity, effluents and waste, transport.

Given this reality, the challenge is not restricted to the analysis of environmental practices that affect the ecosystem, such as the ozone layer, loss of biodiversity, toxic pollution in the air, in rivers, lakes and soils, with complete depletion of non-renewable natural resources, the productive and commercial activity itself will be compromised.

Table 4 presents the socialspectos of GRI G4 and their respective indicators.

Table 4 - Social aspects and respective indicators of the GRI G4 version of 2013

|

Social Aspects |

Social Indicators |

Acronyms |

|

Employment |

New employee hires and turnover by age group and gender |

LA1 |

|

Benefits granted to full-time employees |

LA2 |

|

|

Return to work and retention after maternity/paternity leave |

LA3 |

|

|

Labor Relations |

Minimum notification period on operational changes and whether they are specified in collective bargaining agreements |

LA4 |

|

Health and Safety at Work |

Employees represented in formal health and safety committees |

LA5 |

|

Injuries, occupational diseases, lost days, absenteeism and number of work-related deaths |

LA6 |

|

|

Employees with high incidence or high risk of occupational diseases |

LA7 |

|

|

Health and safety covered by formal agreements with the category |

LA8 |

|

|

Training and Education |

Employee training broken down by gender and functional category |

LA9 |

|

Skills management and continuing learning programmes |

LA10 |

|

|

Employees receiving performance and career analysis |

LA11 |

|

|

Diversity and Equal Opportunities |

Composition of groups responsible for governance indicating the participation of genders and minorities |

LA12 |

|

Equal Pay |

Mathematical ratio of salary and remuneration between men and women |

LA13 |

|

Supplier Evaluation and Labor Practices |

New selected suppliers that respect labor practices |

LA14 |

|

Real and potential negative impacts on labor practices in the supply chain and measures taken in this regard |

LA15 |

|

|

Complaints in Labor Practices |

Number of complaints related to registered, processed and resolved labor practices through a formal mechanism |

LA16 |

|

Investments (Human Rights) |

Agreements and contracts including human rights clauses |

HR1 |

|

Human rights employee training |

HR2 |

|

|

Non-Discriminated |

Total number of cases of discrimination and corrective measures taken |

HR3 |

|

Freedom of Association and Collective Bargaining |

Support of the company to the right of trade union association and collective bargaining of employees |

HR4 |

|

Child labour |

Measures taken to eradicate child labour |

HR5 |

|

Forced Or Slave-Like Labor |

Measures taken to eradicate forced or slave-like labour |

HR6 |

|

Security Practices |

Training of people in the area of human rights security |

HR7 |

|

Indigenous Rights |

Cases of violation of the rights of indigenous peoples and measures taken |

HR8 |

|

Evaluations |

Business operations subject to human rights analysis |

HR9 |

|

Human Rights Supplier Assessments |

New suppliers selected based on human rights criteria |

HR10 |

|

Negative impacts on human rights on the supply chain and containment measures taken |

HR11 |

|

|

Human Rights Complaints and Complaints |

Number of complaints and complaints related to human rights registered, processed and resolved through a formal mechanism |

HR12 |

|

Local Communities (Society) |

Local community engagement and local development |

SO1 |

|

Real and potential negative impacts on local communities |

SO2 |

|

|

Combating Corruption |

Assessment of corruption-related risks and identified risks |

SO3 |

|

Training in anti-corruption policies and procedures |

SO4 |

|

|

Confirmed cases of corruption and measures taken |

SO5 |

|

|

Public Policies |

Financial contributions to political parties |

SO6 |

|

Unfair competition |

Lawsuits arising from unfair competition and trust practices |

SO7 |

|

Compliance |

Fines received as a result of non-compliance with applicable laws |

SO8 |

|

Suppliers and Society |

Selection of suppliers who respect society |

SO9 |

|

Negative impacts from suppliers who do not respect society |

SO10 |

|

|

Society's Complaints |

Settlement of complaints concerning suppliers who disrespect society |

SO11 |

Source: Elaborated by the authors based on GRI (2013).

In the GRI booklet, each indicator indicated in table 4 is followed by an explanatory text, which makes it easier to identify whether or not the company is in line with the GRI booklet. Table 5 presents the results of practices related to the social dimension in the companies surveyed, as recorded in the sustainability reports. The green colors point to the indicators that are in line with the GRI booklet, version 4, of 2013. The highlights in red point to the indicators that are not included in the company's report and are therefore in disagreement with the GRI booklet.

Table 5 - Identification of the practices adopted by companies in the social dimension, in line with the GRI booklet.

|

Social Aspects of GRI G4 |

Acronyms of Indicators |

Identification of Social Indicators in Reports |

|||||||||

|

BR Distribuidora |

Braskem |

Bunge |

Cargill |

Carrefour |

Ipiranga |

Petrobrás |

Raízen |

Vale |

Vivo |

||

|

Employment |

LA1 |

|

|

|

|

|

|

|

|

|

|

|

LA2 |

|

|

|

|

|

|

|

|

|

|

|

|

LA3 |

|

|

|

|

|

|

|

|

|

|

|

|

Labor Relations |

LA4 |

|

|

|

|

|

|

|

|

|

|

|

Health and Safety at Work |

LA5 |

|

|

|

|

|

|

|

|

|

|

|

LA6 |

|

|

|

|

|

|

|

|

|

|

|

|

LA7 |

|

|

|

|

|

|

|

|

|

|

|

|

LA8 |

|

|

|

|

|

|

|

|

|

|

|

|

Training and Education |

LA9 |

|

|

|

|

|

|

|

|

|

|

|

LA10 |

|

|

|

|

|

|

|

|

|

|

|

|

LA11 |

|

|

|

|

|

|

|

|

|

|

|

|

Equal Opportunities |

LA12 |

|

|

|

|

|

|

|

|

|

|

|

Equal Pay |

LA13 |

|

|

|

|

|

|

|

|

|

|

|

Supplier Evaluation and Labor Practices |

LA14 |

|

|

|

|

|

|

|

|

|

|

|

LA15 |

|

|

|

|

|

|

|

|

|

|

|

|

Complaints Labor Practices |

LA16 |

|

|

|

|

|

|

|

|

|

|

|

Investments (Human Rights) |

HR1 |

|

|

|

|

|

|

|

|

|

|

|

HR2 |

|

|

|

|

|

|

|

|

|

|

|

|

Non-Discriminated |

HR3 |

|

|

|

|

|

|

|

|

|

|

|

Association and Collective Bargaining |

HR4 |

|

|

|

|

|

|

|

|

|

|

|

Child labour |

HR5 |

|

|

|

|

|

|

|

|

|

|

|

Forced or Slave Labor |

HR6 |

|

|

|

|

|

|

|

|

|

|

|

Security Practices |

HR7 |

|

|

|

|

|

|

|

|

|

|

|

Indigenous Rights |

HR8 |

|

|

|

|

|

|

|

|

|

|

|

Evaluations |

HR9 |

|

|

|

|

|

|

|

|

|

|

|

Human Rights Supplier Assessments |

HR10 |

|

|

|

|

|

|

|

|

|

|

|

HR11 |

|

|

|

|

|

|

|

|

|

|

|

|

Human Rights Complaints |

HR12 |

|

|

|

|

|

|

|

|

|

|

|

Local Communities (Society) |

SO1 |

|

|

|

|

|

|

|

|

|

|

|

SO2 |

|

|

|

|

|

|

|

|

|

|

|

|

Combating Corruption |

SO3 |

|

|

|

|

|

|

|

|

|

|

|

SO4 |

|

|

|

|

|

|

|

|

|

|

|

|

SO5 |

|

|

|

|

|

|

|

|

|

|

|

|

Public Policies |

SO6 |

|

|

|

|

|

|

|

|

|

|

|

Unfair competition |

SO7 |

|

|

|

|

|

|

|

|

|

|

|

Compliance |

SO8 |

|

|

|

|

|

|

|

|

|

|

|

Supplier Evaluation (Company) |

SO9 |

|

|

|

|

|

|

|

|

|

|

|

SO10 |

|

|

|

|

|

|

|

|

|

|

|

|

Complaints Society |

SO11 |

|

|

|

|

|

|

|

|

|

|

Source: Elaborated by the authors based on the research data.

From Table 5, it can be seen which companies showed good or bad performance. The companies that obtained good use in this dimension were: Petrobras, Vale and Cargill.

The practices evidenced by the indicators LA5, LA6, LA7, LA16, HR10, HR11, S01, S011 were the best presented, being perceived in all selected companies. The categories "Local Communities", "Fight against Corruption", "Supplier Evaluation in Human Rights" and "Health and Safety at Work" stand out, which had the best benefits.

On the other hand, indicators L3, L4, HR1 and SO7 apparently did not receive much attention in the reports, since the analysis showed very low utilization by organizations. However, it is a number considered low compared to the number of practices of this dimension. Within the categories, the ones that were least evidenced are "Unfair Competition" and "Employment".

Table 6 presents the indicators related to GRI G4 economic aspects and their respective indicators.

Table 6 - Economic aspects and indicators of GRI g4 version of 2013.

|

Economic Aspects |

Economic Indicators |

Acronyms |

|

Economic Performance |

Direct economic value generated and distributed |

EC1 |

|

Financial implications and other risks and opportunities for the organization's activities due to climate change |

EC2 |

|

|

Coverage of benefit pension plan obligations defined offered by the organization |

EC3 |

|

|

Financial assistance received from the government |

EC4 |

|

|

Presence in the Market |

Change in the proportion of the lowest wage compared to the local minimum wage in important operating units |

EC5 |

|

Proportion of senior management members hired in the local community in important operational units |

EC6 |

|

|

Indirect Economic Impacts |

Development and impact of investments in infrastructure and services offered |

EC7 |

|

Significant indirect economic impacts, including the extent of impacts |

EC8 |

|

|

Purchasing Practices |

Proportion of spending on local suppliers in important operating units |

EC9 |

Source: Prepared by the authors based on GRI (2013).

In the GRI booklet, each indicator presented in Table 6 is followed by an explanatory text that makes it easier to identify whether or not the company is in line with the GRI booklet. Table 7 presents the results of the economic dimension in the companies surveyed, according to the sustainability reports. The green colors point to indicators that are in line with the GRI booklet, version 4, of 2013. Red colors represent the indicators that are not included in the company's report and are therefore in disagreement with the GRI booklet.

Table 7 - Identification of the practices adopted by companies in the economic dimension, in line with the GRI booklet.

|

Economic Aspects of GRI G4 |

Acronyms of Indicators |

Identification of Economic Indicators in Reports |

|||||||||

|

BR Distribuidora |

Braskem |

Bunge |

Cargill |

Carrefour |

Ipiranga |

Petrobrás |

Raízen |

Vale |

Vivo |

||

|

Economic Performance |

EC1 |

|

|

|

|

|

|

|

|

|

|

|

EC2 |

|

|

|

|

|

|

|

|

|

|

|

|

EC3 |

|

|

|

|

|

|

|

|

|

|

|

|

EC4 |

|

|

|

|

|

|

|

|

|

|

|

|

Presence in the Market |

EC5 |

|

|

|

|

|

|

|

|

|

|

|

EC6 |

|

|

|

|

|

|

|

|

|

|

|

|

Indirect Economic Impacts |

EC7 |

|

|

|

|

|

|

|

|

|

|

|

EC8 |

|

|

|

|

|

|

|

|

|

|

|

|

Purchasing Practices |

EC9 |

|

|

|

|

|

|

|

|

|

|

Source: Elaborated by the authors based on the research data.

According to the analysis of the reports, with the selected indicators, the companies that stood out in the economic dimension were: Petrobras, Vale and Braskem.

The EC1, EC7, EC8 practices received special attention, considering that the EC8 guideline was the only one that was present in all ten reports. The categories "Indirect Economic Impacts" and "Economic Performance" were the ones that had a better use.

On the other hand, the EC3 and EC9 guidelines did not obtain good results in terms of practices related to the economic dimension, showing little expressiveness in the analyzed reports. However, it is a number considered low, being only two out of a total of nine. Regarding the categories, the least used was "Purchasing Practices", however, only four companies did not evidence actions in this sense. It is the smallest category, compared to the other.

Table 8 presents a summary of the situation of each company in relation to the economic, social and environmental dimensions. The green color indicates that the company's report concentrates elements related to environmental sustainability, indicating an adherence above 50%.

The red color indicates that the company's report gathers few elements in the field of sustainability, indicating an adherence below 50%.

Table 8 - Adherence of companies to the dimensions of sustainability.

|

Enterprise |

Environmental |

Social |

Economic |

|

BR Distributor |

|

|

|

|

Braskem |

|

|

|

|

Bunge |

|

|

|

|

Cargill |

|

|

|

|

Carrefour |

|

|

|

|

Ipiranga |

|

|

|

|

Petrobras |

|

|

|

|

Raízen |

|

|

|

|

Vale |

|

|

|

|

Vivo |

|

|

|

Source: Elaborated by the authors based on the research data.

The environmental issue has occupied considerable space in the projects of companies. It is a perspective that corroborates the idea of there being a growing predilection of the industrial sector to take care of the environment. It is the participation of large industries in the agro-industrial, energy and chemical sectors in the enumeration of selected organizations, that is, branches marked by significant impacts on ecosystems, thus lighting a warning light for the environmental pillar of sustainability.

In view of the GRI guidelines, applied to the ten companies mentioned, only one did not clearly present its economic dimension, while five companies did not present enough information to demonstrate environmental sustainability actions in their activities. In this context, addressing nature conservation in the light of human interests and an anthropocentric logic, Gudynas (2019, p. 283) criticizes the acceptance of "benevolent capitalism, in which corporations, together with local governments and communities, will solve environmental problems". This positioning reveals a critical view about the role of the respective type of development and its possible connection with the environmental problem in question. It is a way to increase environmental practices in the organizations addressed.

The results reveal that five of the companies analyzed demonstrate to follow the guidelines of the booklet in terms of sustainability. They are: Braskem, Cargill, Carrefour, Petrobrás and Vale.

Studies conducted by Brown, Jong and Levy (2009), Leite Filho, Prates and Guimarães (2009), Ribeiro et al. (2009), Campos et al. (2013) and Madalena et al. (2016) also sought to identify the level of evidence of socio-environmental information in sustainability reports in Brazilian companies. Like this study, they also showed that a significant part of the companies, in several aspects analyzed, did not meet the recommendations of the GRI standard.

The study by Leite Filho, Prates and Guimarães (2009) shows that, despite the fact that the reports of the companies surveyed are comprehensive, covering almost all the aspects requested by the GRI guidelines, there is a clear lack of parameterization involving both the form of presentation of the report and the evidence of its content. These deficiencies found in the reports end up becoming barriers for users to have access to the information they need. The research by Ribeiro et al. (2009) revealed that, because GRI suggests the contents and does not impose the standards, this allows to be significant differences even between companies that adopt the same booklet. For Campos et al. (2013, p. 918) the "lack of standardization in the disclosure of information" may act as a barrier "preventing other companies from benchmarking the organization that is disclosing its indicators".

Campos et al. (2013) and Madalena et al. (2016) argue that there are still a large number of organizations that publish their reports without declaring the level of adherence to the GRI Indicators Guidelines. There is also a lack of structuring or lack of interest of companies, to meet the recommendations regarding the profile of the report, the characterization of the companies and the scenario in which they operate.

The studies conducted by Campos et al. (2013) and Madalena et al. (2106) reveal that organizations have sought greater adaptation to the increasing levels of demands regarding the dissemination and transparency of sustainability indicators present in their reports. The result of the study in question corroborates this result. However, it was verified in both studies that in recent years there has been little evolution regarding the attendance of the parameters established by the GRI booklet. Therefore, these researches show that there are still improvements to be made by organizations to achieve excellence in the publication of sustainable information.

For sure there are criticisms directed at the GRI booklet. However, the contributions to organizations in general are undeniable (BROWN; Jong; LEVY, 2009; CAMPOS et al., 2013). Thus, it can be said that the contributions of the GRI report to organizations consists of: (i) leading the organization to adopt performance indicators that represent a concept of sustainability supported by the Triple Bottom Line, (ii) from the perspective that an ethical company does not adopt the practice of greenwashing, the performance indicators presented in the report allow stakeholders to know the (in)sustainable actions of the organization taking into account the principle of transparency, (iii) by showing the weaknesses existing in the organization, they can serve as parameters for the corrective actions necessary to better meet the requirements of an increasingly conscious society, (iv) the indicators presented in the sustainability report allow the organization's conformities and non-conformities to be verified through external audits.

Sustainable development and sustainable practices offer the possibility of a special increase in human well-being, without extrapolating the biophysical limits of the planet. In addition, they figure as competitive factors, reorienting the performance of the private sector and reshaping business species of organizations, allowing their activities not, in fact, to be harmful to people and the balance of life on the planet.

In this context, the sustainability report emerges as an important element. However, presenting it annually does not transform the company into an automatically sustainable organization. It is necessary to put into practice everything that has been verified, with regard to improvements and changes, seeking to cause the least impact to the environment and the greatest social and economic impact.

After analyzing the sustainability reports of large Brazilian companies, it is noticed that some GRI guidelines were achieved. However, it is perceived that there is also a challenge to be faced by organizations, especially with regard to the environmental dimension, which constitutes the basis of all social and economic relations.

Despite the advances perceived in recent years and through the sustainability reports of companies, a decided and true conversion to genuinely sustainable development is mandatory. This may favor the implementation of good practices capable of responding to the main challenges of the 21st Century.

The authors thank CNPq for the financial support for this research.

ABRAMOVAY, R. Muito além da Economia Verde. São Paulo: Abril, 2012.

BARAIBAR-DIEZ, E; SOTORRIO, L. L. O efeito mediador da transparência na relação entre responsabilidade social corporativa e reputação corporativa. Revista Brasileira de Gestão e Negócios, v. 20, n. 1, p. 5-21, 2018. https://doi.org/10.7819/rbgn.v20i1.3600

BARBIER, E. B. The concept of sustainable economic development. Environmental Conservation, v. 14, n.2, p.101-110, jun. 1987. https://doi.org/10.1017/S0376892900011449

BARDIN, L. Análise de conteúdo. 4. Ed. São Paulo: Edições70, 2016.

BRADFORD, M.; EARP, J.; WILLIAMS, P. Sustainability reports: what do stakeholders really want? Management Accounting Quarterly, v. 16, n. 1, p. 13-18, 2014. Avalilable in: https://www.imanet.org/-/media/96272aa5f09148f9b48090dbede95e86.ashx. Accessed in: 15 fev. 2021.

BROWN, H. S.; JONG, M.; LEVY, D. L. Building institutions based on information disclosure: lessons from GRI’s sustainability reporting. Journal of Cleaner Production, v. 17, p. 571-580, 2009. http://dx.doi. org/10.1016/j.jclepro.2008.12.009

CAMPOS, L. M. S. et al. Relatório de sustentabilidade: perfil das organizações brasileiras e estrangeiras segundo o padrão da Global Reporting Initiative. Gestão & Produção, v, 20, n. 4, p. 913-926, 2013. https://dx.doi.org/10.1590/S0104-530X2013005000013

CASTRO, A. E; CAMPOS, S. A. P; TREVISAN, M. A institucionalização (ou banalização) da sustentabilidade organizacional à luz da teoria crítica. Revista Pensamento Contemporâneo em Administração, v, 12, n. 3, p. 110-123, 2018. https://doi.org/10.12712/rpca.v12i3.12552

COOPER, D. R.; SCHINDLER, P. S. Métodos de pesquisa em administração. 12. ed. Porto Alegre: Bookman, 2016.

CONSTANZA, R.; PATTERN, B. C. Defining and Predicting Sustainability. Ecological Economics, v. 15, n.3, p.193-195, dez. 1995. https://doi.org/10.1016/0921-8009(95)00048-8

ELKINGTON, J. Sustentabilidade, canibais de garfo e faca. São Paulo: Makron Books, 2012.

FEIL, A. A.; STRASBURG, V. J.; NAIME, R. H. Análise sobre as normas e dos indicadores de sustentabilidade e a sua integração para gestão corporativa. Perspectivas em Gestão & Conhecimento, v. 3, n. 2, p. 21-36, 2013. Avalilable in: https://periodicos.ufpb.br/ojs/index.php/pgc/article/view/16349/9995. Accessed in: 08 mar. 20221.

FONSECA, A. et al. The state of sustainability reporting at Canadian universities. International Journal of Sustainability in Higher Education, v. 12, n. 1, p. 22-40, 2011. https://doi.org/10.1108/14676371111098285

GIL, A. C. Métodos e técnicas de pesquisa social. 7. ed. São Paulo: Atlas, 2019.

GRI – GLOBAL REPORTING INITIATIVE. Diretrizes para relatório de sustentabilidade. Versão G4. Amsterdã: GRI, 2013. Avalilable in: http://www.globalreporting.org. Accessed in: 22 fev. 2021.

GUDYNAS, E. Direitos da Natureza: Ética biocêntrica e políticas ambientais. São Paulo: Elefante Editora, 2019.

INSTITUTO ETHOS de Empresas e Responsabilidade Social. Indicadores ETHOS de Responsabilidade Social. 2014. Avalilable in: http://www.ethos.org.br. Accessed in: 14 set. 2018.

LEITE FILHO, G. A.; PRATES, L. A.; GUIMARÃES, T. N. Níveis de Evidenciação dos Relatórios de Sustentabilidade das Empresas Brasileiras A+ do Global Reporting Initiative (GRI) no Ano de 2007. RCO – Revista de Contabilidade e Organizações – FEA-RP/USP, v. 3, n. 7, p. 43-59, set-dez 2009. https://doi.org/10.11606/rco.v3i7.34749

LOZANO, R. Envisioning sustainability three-dimensionally. Journal of Cleaner Production, v. 16, n. 17, p. 1838-1846, nov. 2008. https://doi.org/10.1016/j.jclepro.2008.02.008

LOURENÇO; M. A.; CARVALHO, D. Sustentabilidade social e desenvolvimento sustentável. RACE, v. 12, p. 1, p. 9-38, 2013. Avalilable in: https://portalperiodicos.unoesc.edu.br/race/article/view/2346. Accessed in: 14. set. 2018.

MADALENA, J. D. et al. Estudo dos Relatórios de Sustentabilidade GRI de Empresas Brasileiras. REGET - Revista Eletrônica em Gestão, Educação e Tecnologia Ambiental, Santa Maria, v. 20, n. 1, p. 566−579, jan.-abr. 2016. https://doi.org/105902/22361170 20021

MARIMON, F. et al. The worldwide diffusion of the Global Reporting Initiative: what is the point? Journal of Cleaner Production, v. 33, p. 132-144, 2012. https://doi.org/10.1016/j.jclepro.2012.04.017

MMA – MINISTÉRIO DO MEIO AMBIENTE. Agenda 21 brasileira: Ações prioritárias. Brasília: MMA, 2004.

MOZZATO, A. R.; GRZYBOVSKI, D. Análise de conteúdo como técnica de análise de dados qualitativos no campo da administração. Revista de Administração Contemporânea, v. 15, n. 4, p. 731-747, jul./ago. 2011. https://doi.org/10.1590/S1415-65552011000400010

NASCIMENTO, L. F.; LEMOS, Â. D.; MELLO, M. C. A. Gestão socioambiental estratégica. Porto Alegre: Bookman, 2008.

NAVARRETE, J. M. Sobre la investigación cualitativa: Nuevos conceptos y campos de desarrollo. Investigaciones Sociales, v. 8, n. 13, p. 277-299, 2004. https://doi.org/10.15381/is.v8i13.6928

NEVES, L. F. Diagnóstico da institucionalização da responsabilidade social corporativa em empresas da Região Metropolitana de Campinas – SP. 2019. 115 f. Dissertação (Mestrado em Sustentabilidade) – PUC-Campinas, Campinas, 2019.

NETO, S. M.; PEREIRA, M. F.; MORITZ, G. O. Novo capitalismo: criação de valor compartilhado e responsabilidade social empresarial. Revista Pretexto, v. 13, n. 3, p. 72-91, 2012. https://doi.org/10.21714/pretexto.v13i3.1260

OLIVEIRA, M. M. Como fazer pesquisa qualitativa. 7. ed. Petrópolis, Vozes, 2016.

OLIVEIRA, L. R. et al. Sustentabilidade: da evolução dos conceitos à implementação como estratégia nas organizações. Produção, v. 22, n. 1, p. 70-82, 2012. http://dx.doi.org/10.1590/S0103-65132011005000062

ONU. Report of the World Commission on Environment and Development. 1987. Avalilable in: http://www.un.org/documents/ga/res/42/ares42-187.htm. Accessed in: 16 abr. 2018.

PAZ, F. J.; KIPPER, L. M. Sustentabilidade nas organizações: vantagens e desafios. GEPROS, v. 11, n. 2, p. 85-102, 2016. https://doi.org/10.15675/gepros.v11i2.1403

PORTAL ESTADÃO. Ranking 1500. 2019. Avalilable in: https://publicacoes.estadao.com.br/ empresasmais2019/ranking-1500/. Accessed in: 06 mar. 2021.

RIBEIRO, M. S. et al. Responsabilidade socioambiental no setor de papel e celulose. In: ENCONTRO DA ASSOCIAÇÃO NACIONAL DE PÓS-GRADUAÇÃO E PESQUISA EM ADMINISTRAÇÃO, 33., 2009, São Paulo. Anais..., São Paulo: ANPAD, 2009.

RICHARDSON, R. J. Pesquisa Social: Métodos e Técnicas. 4. ed. São Paulo: Atlas, 2017.

ROGERS, P. P; KAZI, F; BOYD, J. A. An introduction to sustainable development. Londres: Earthscan, 2008.

ROHRICH, S. S.; TAKAHASHI, A. R. W. Sustentabilidade ambiental em Instituições de Ensino Superior: um estudo bibliométrico sobre as publicações nacionais. Gestão & Produção, v. 26, n. 2, e2861, 2019. https://dx.doi.org/10.1590/0104-530x2861-19

SACHS, I. Caminhos para o desenvolvimento sustentável. Rio de Janeiro: Garamond, 2002.

SARKIS, J.; HELMS, M. M.; HERVANI, A. A. Reverse logistics and social sustainability. Corporate Social Responsibility and Environmental Management, v. 17, n. 6, p. 337-354, 2010. https://doi.org/10.1002/csr.220

SEN, A. Desenvolvimento como liberdade. São Paulo: Companhia das Letras, 2010.

SILVA, L. H. V. Aplicação e impactos dos objetivos de desenvolvimento sustentável em grandes empresas privadas do setor industrial no Brasil. 2021. 157 f. Dissertação (Mestrado em Sustentabilidade) – Pontifícia Universidade Católica de Campinas, Campinas, 2021.

SOUZA, T. C. G. Relatório de sustentabilidade: proposta de aplicação em uma instituição de ensino superior comunitária à luz da Global Reporting Initiative (GRI). 2018. 152 f. Dissertação (Mestrado em Sustentabilidade) – PUC-ampinas, Campinas, 2018.

VAN BELLEN, H. M. Indicadores de sustentabilidade: uma análise comparativa. 3. ed. Rio de Janeiro: FGV, 2008.

VIFELL, A. C.; SONERYD, L. Organizing matters: how ‘the social dimension’ gets lost in sustainability projects. Sustainable Development, v. 20, n. 20, p. 18-27, 2012. https://doi.org/10.1002/sd.461