Aloisio Pereira Júnior - E-mail: aloisio@iftm.edu.br, Orcid: aloisio@iftm.edu.br, Afiliação institucional: Instituto Federal do Triângulo Mineiro - Patrocínio - MG – Brasil, Titulação: Doutor em Administração pela Universidade Federal de Uberlândia (UFU), professor no Instituto Federal do Triângulo Mineiro (IFTM), Patrocínio-MG.

Vinicius Silva Pereira - E-mail: viniciuss56@ufu.b, Orcid: https://orcid.org/0000-0002-4521-9343, Afiliação institucional: Federal University of Uberlândia - Uberlândia - MG – Brasil, Titulação: Doutor em Administração (FGV), Professor na Faculdade de Gestão e Negócios (UFU), Uberlândia-MG.

Summary

The study of the effects of geographic diversification within the same country on the performance of firms is still incipient in the literature. The concepts of international business literature and economic geography are applied to this research in the analysis of this relation. The objective is to analyze the effect of the determinants of the location of subnational regions and cash on the financial and operational performance of Brazilian companies listed on B3, according to the location of their subsidiaries. Multiple linear regressions were performed with data for the year 2020 to verify the relation between the research object of analysis. The results show that the interaction between cash and market size of the company's subsidiary's location is related to its financial performance. It was also verified that the market size and the sustainable development of the company's headquarters location are negatively and positively associated, respectively, with the operational performance of the companies in the sample. The research contributes to the theory by expanding the studies of the effects of regional diversification on companies' results, applying the concepts of international diversification in the study of the effects of regional diversification on companies' performance, which is still emerging in the literature.

Keywords: region; location determinants; cash; performance.

The appreciation of the region has contributed to the academic environment to discuss conceptual and theoretical aspects of the region, regionalism and regionality (Gil, 2007). It was a field of study restricted to Geography, but it has been gaining space in other fields of study, including Administration, but courses and publications related to the influence of the region on its object of study are still incipient (GIL; OLIVA; SILVA, 2007).

The concept of the region has been constructed from the perspective of several aspects, such as the predominance and evasion of regional productive factors, local demands, common enterprises and competitiveness (GIL, KLINK; SANTOS, 2004 apud GIL; OLIVA; GASPAR, 2007). Regionality may be seen as a set of economic and historical elements that differentiate a given region, allowing comparisons between regions (GIL; OLIVA; GASPAR, 2007).

In the context of international business, for a long time, research in the area of international geographic diversification assumed the homogeneity of the host country in the study of internationalization strategies and their consequences, as well as the modes of entry and the location options of subsidiaries (HUTZSCHENREUTER; MATT; KLEINDIENST, 2020). However, more and more international diversification strategy is being considered at the subnational level (HUTZSCHENREUTER; MATT; KLEINDIENST, 2020).

A subnational region may be conceptualized as a space within a country and is usually demarcated by a cultural, economic and administrative border, such as a federal state or a province (HUTZSCHENREUTER; MATT; KLEINDIENST, 2020). Previous studies have found variations of subnational regions in terms of culture, institutions, natural resources and other geographic and economic features (BEUGELSDIJK & MUDAMBI, 2013; CASTELLANI, GIANGASPERO AND ZANFEI, 2013; SUN; PENG; LEE; TAN, 2015).

Due to the heterogeneity of subnational regions, firm performance is related to different location-specific subnational advantages (CHIDLOW et al., 2015; SLANGEN, 2016). In a recent study, Oliveira (2020) analyzed the effects of subnational location determinants on the performance of subsidiaries located in Latin America. In the study, the author verifies whether the determinants of subnational location, such as market size, market attractiveness, human capital and socioeconomic development influence the operational and financial performance of the analyzed subsidiaries.

In this sense, previous researches have not investigated the effects of geographic diversification within the same country on the performance of companies, considering the determinants of the location of the subnational regions in which their subsidiaries are located. The present study aims to apply the perspectives of international diversification at the subnational level in the context of the diversification of Brazilian companies to different regions of Brazil since those have different geographic, cultural, institutional and economic characteristics that may offer unique advantages and challenges for performance, finance and operations of companies.

From the perspective of Contingency theory, the way in which the company combines its resources with the environment influences its performance, and its effectiveness is associated with the conformity of its internal features and external contingencies (DRAZIN; VAN de VEN, 1985; JUNG; FOEGE; NUESCH, 2020; WANG; SINGH, 2014). In addition, establishing an intersection with the Contingency Theory, the Resource-Based View Theory (RBV) points out that the way in which the company uses its resources may guarantee growth and competitive advantage (BARNEY, 1991; PENROSE, 1959; WERNERFELT, 1984).

Based on the RBV Penrosean logic (1959) that the versatility of resources allows companies to recombine them in different ways, enabling a range of services that may contribute to their growth, it is argued that the cash, for being versatile, is a valuable resource (JUNG; FOEGE; NUESCH, 2020), which, associated with the determining factors of subnational regions, may contribute to a better performance.

From this perspective, Jung, Foege and Nuesch (2020) show that cash is a valuable resource for the company to promote the strategic adjustment to the environment in which it operates. How it strategically manages its cash given the locational determinants of the subnational regions in which it operates, it may influence its performance.

In this sense, it is questioned what is the effect of the determinants of the location of subnational regions and cash on the financial and operational performance of Brazilian companies, considering the differences in economic factors and market size between regions.

Therefore, the objective of this paper is to verify whether the interaction of cash with the determinants of the location of the subnational regions of the subsidiary's city influences the performance of Brazilian companies listed on B3, according to the location of its subsidiary(ies). As a complementary analysis, this research seeks to identify whether the determinants of location in the subnational regions where companies are headquartered are associated with performance. Data analysis was performed using multiple linear regressions using the Generalized Least Squares (GLS) method.

The research contributes to the theory by expanding the studies of the effects of regional diversification on firm performance, applying the concepts of international diversification in the study of the effects of regional diversification on performance, which is still emerging in the literature. The research also contributes by analyzing performance in terms of the determinants of the location of subnational regions and cash, projecting light on understanding how regional diversification and liquidity may contribute to performance. With this study, it is possible to identify the most suitable regions/environments for companies to diversify their businesses, since regions with greater sustainable development may be potential destinations for investments and business activities.

The appreciation of the region has contributed to the academic environment to discuss conceptual and theoretical aspects of the region, regionalism and regionality (GIL, 2007). It was a field of study restricted to Geography, but which is currently discussed in Economics, Sociology, Health, Urbanism and Administration. In the field of Administration, courses and publications related to the influence of the region on its object of study are still incipient (GIL; OLIVA; SILVA, 2007).

Currently, the concept of the region has been constructed from the perspective of several aspects, such as the predominance and evasion of regional productive factors, local demands, common enterprises and competitiveness (GIL, KLINK; SANTOS, 2004 apud GIL; OLIVA; GASPAR, 2007). Regionality may be seen as a set of economic and historical elements that differentiate a given region, allowing comparisons between regions (GIL; OLIVA; GASPAR, 2007).

Traditional research on strategic management has over time been dominated by the perspective that industry structure (industrial organization economics perspective) and firm resources and capabilities (RBV perspective) are key determinants of organizational performance (CHAN; MAKINO; ISOBE, 2010). In addition, conventional studies of international business that are anchored in theories of trade and Economic Geography argue that the specific factors of the host country are critical determinants of organizational performance (CHAN; MAKINO; ISOBE, 2010). Those studies generally suggest that differences in country, industry, and firm attributes explain variation in firm performance (CHAN; MAKINO; ISOBE, 2010).

For a long time, most international business researchers assumed that countries would be homogeneous within their national borders. Location in international business is almost always conceptualized and operationalized at the country level, the very term “international business” invokes the nation-state as a unit of analysis (BEUGELSDIJK & MUDAMBI, 2013). However, international strategy is increasingly being observed at the subnational level (CASTELLANI; GIANGASPERO; ZANFEI, 2013; HUTZSCHENREUTER; MATT; KLEINDIENST, 2020).

A subnational region may be conceptualized as a space within a country and is usually demarcated by a cultural, economic and administrative border, such as a federal state or a province (HUTZSCHENREUTER; MATT; KLEINDIENST, 2020). By analyzing the behavior of regional diversification within the country itself, the present paper applies the geographical vision of a region, which according to Chidlow et al. (2015) is a region within a particular nation. Also according to those authors, the geographical view is adequate for studies of the subsidiaries’ location.

Studies in Economic Geography show that there are significant economic differences within national borders, therefore the country is not the lowest level of analysis of the location of subsidiaries, as countries are not homogeneous and there are variations between subnational regions in terms of culture, institutions, natural resources and other geographic and economic features (BEUGELSDIJK; MUDAMBI, 2013; CASTELLANI, GIANGASPERO; ZANFEI, 2013; CHIDLOW et al., 2015; SUN et al., 2015). According to Chan, Makino and Isobe (2010), regional variation, especially in emerging economies, originates from continuous and incremental institutional changes, uneven economic development and cultural and ethnic diversity.

Due to the heterogeneity of the local context of the subnational regions, the performance of companies is related to the different subnational advantages specific to location, which, in their turn, are linked to dimensions such as agglomeration, infrastructure, efficiency, market size, quality of formal institutions and cultural and knowledge factors that may be differentiated between regions (CHIDLOW et al., 2015; OLIVEIRA, 2020; SLANGEN, 2016). That view of the heterogeneity of regions within the country adds the dimensions of subnational regions as an important unit of analysis for the determinants of firm performance.

According to Meyer and Nguyen (2005), foreign companies are located in subnational regions where institutions are more favorable to their business and where institutional barriers inhibit their access to local resources. The heterogeneity of subnational regions may provide differentiated opportunities and restrictions to subsidiaries, whose effects are important in explaining the variation in the performance of multinationals and their subsidiaries (CHIDLOW et al., 2015; OLIVEIRA, 2020).

Chan, Makino and Isobe (2010) found that features of the subnational region have an effect on the variation in the performance of subsidiaries of foreign companies. Those authors found that the subnational regions of the USA and China, host countries, are important in explaining the performance of foreign affiliates, demonstrating that the subnational region represents an additional level of performance analysis.

Ma, Tong and Fitza (2013) also argue that the effect of the subnational region on the performance of the foreign subsidiary derives from its insertion in the local context of the host country, as those contexts in a large emerging economy may vary significantly in its subnational regions regarding factors of production, institutions, industrial agglomerations, infrastructure, efficiency and knowledge factors (CHIDLOW et al., 2015).

The strategic alignment of subsidiaries to local features may contribute to better performance. Institutional and economic characteristics of the host country's environment have a relevant direct effect on the survival and growth of foreign firms (LUO; PARK, 2001). Luo and Park (2001) showed that multinational companies, whose strategies are properly aligned with different local environments, are more likely to achieve superior performance in emerging economies, such as China, for example.

According to Hutzschenreuter, Matt and Kleindienst (2020), most previous researches have concentrated studies on subnational regions of large European countries, the USA and China. Research in that area should also focus on emerging countries other than China, investigating the substantial variation between regions within each country, such as Brazil, which is a country of almost continental size (CASTELLANI; GIANGASPERO; ZANFEI, 2013; HUTZSCHENREUTER; MATT; KLEINDIENST, 2020).

Including the Brazilian context, Oliveira (2020) analyzed the effects of subnational location determinants on institutional distance and the performance of subsidiaries located in Latin America. The study identified that among the determinants of subnational location, socioeconomic development directly influences the performance of the analyzed subsidiaries.

For all of the above, it is argued, therefore, that due to the heterogeneity of the local context of subnational regions within an economy, the financial and operational performance of companies is associated with factors of the subnational region, that is, location-specific subnational advantages of its subsidiaries.

From a contingency perspective, the environment, in the case of this study, the subnational region in which the subsidiary is located, influences its performance, and the company's effectiveness is associated with the compliance of its internal features and external contingencies (DRAZIN; VAN de VEN, 1985; JUNG; FOEGE; NUESCH, 2020; WANG; SINGH, 2014).

In this way, the Contingency theory and the VBR theory contribute to the understanding of the effects of the conditions of the geographic environment, in this case, the location factors of the subnational regions, as well as the use of resources to guarantee competitive advantage and organizational growth (BARNEY, 1991; PENROSE, 1959).

Based on the Penrosean logic (1959) of RBV, the versatility of resources allows companies to recombine them in different ways, enabling a range of services that may contribute to their growth. The cash, being versatile, is a valuable resource and may offer competitive advantage and growth, in addition of playing a facilitating role in the alignment (strategic fit) of the company with its environment (JUNG; FOEGE; NUESCH, 2020; PENROSE, 1959).

It is argued that the combination of cash and the environment (determinants of the location of subnational regions) influences performance. Following Jung, Foege and Nuesch (2020), the strategic fit is the underlying mechanism for understanding the link between cash and the company's environment. According to those authors, strategic adjustment means combining the entire company, understood as a package of corporate resources, with the environmental contingencies that affect its performance.

If, in the past, having more liquidity was considered an inefficient management choice, nowadays more and more companies decide to accumulate cash reserves as a tool to support business growth and development processes (ROCCA; CAMBREA, 2018), as well as preventive protection against the challenges of the environment (ALMEIDA et al., 2014).

Thus, consider a company "A" headquartered in Brazil whose geographic diversification strategy is to maintain subsidiary(ies) within the country itself, which due to its territorial extension has variations between its subnational regions, it is questioned whether the relative location factors the subnational regions in which the subsidiary operates, associated with the company's liquidity, influence its performance on a consolidated basis. Therefore, the present study seeks to apply the perspectives of international geographic diversification regarding aspects of subnational regions, nevertheless in the context of geographic diversification within the country itself.

As shown, previous researches have focused on the study of variations between subnational regions and their effects on the performance of internationalized companies from the perspective of the location of their subsidiaries in the host country. Nonetheless, according to Farole et al. (2017), the relation between business environment and performance at the subnational level has received less attention, as the subnational business climate has been seen as having less influence on companies.

In more recent research, Farole et al. (2017) demonstrated that overall the business environment affects performance. Those authors found that Italian and Spanish companies located in backward regions had negative effects on their profitability. The results suggest that policies that improve the business environment in lagging regions may benefit the performance of firms located in those regions.

Thus, in addition to investigating the regional diversification of Brazilian companies in terms of the location of their subsidiaries, the present paper also analyzes whether the determinants of the location of the subnational regions where the headquarters are located influence their performance. In the next section, therefore, hypotheses are developed regarding the effects of the determinants of the location of subnational regions and liquidity on firm performance.

Dunning (1998) states the advantages of location are relevant factors in the decision-making of multinationals regarding new places of economic activity. According to that author, the advantages associated with location refer to local factors which include market size, natural resources, human capital, technological development, infrastructure, opportunities for efficiency and economic/political stability. In accordance with RBV, location-specific assets, resources, and factors drive differential advantages linked to that location (HSU; CHEN; CASKEY, 2017).

Previous researches have investigated the relation between location factors and firm performance in the context of the subnational region where subsidiaries are based (CHAN; MAKINO; ISOBE, 2010; MA; TONG; FITZA, 2013; OLIVEIRA, 2020; TENG; HUANG; PAN, 2017). Oliveira (2020), specifically, used four determinants of location: market size, human capital, market attractiveness and socioeconomic development.

In business expansion, it is important to observe the size of the market when deciding on a location. Larger markets may offer greater economies of scale in production and greater profits, since the costs related to familiarization with aspects of the environment, such as laws, language and culture, may be offset by a high volume of sales (MATALONI, 2011).

The size and attractiveness of the market may be measured by the total population of cities or provinces (AMITI; JAVORCIK, 2008) and by the Gross Domestic Product (GDP) of the region/city (TENG; HUANG; PAN, 2017). The higher the GDP, the richer the market, which may optimize the company's performance (SALAH, 2018).

It is understood that countries/regions may increase their attractiveness by adopting policies that increase the level of local qualification and that develop human resources (OLIVEIRA, 2020). Both at the micro and macro levels, higher investments in human capital improve performance at the firm level (OLIVEIRA 2020). Skilled workers may increase the efficiency of the production process (MATALONI, 2011).

The Human Development Index (HDI) is used as a measure of socioeconomic development that includes not only the level of education but also health and income. Salah (2018) points to a statistically significant relation between the HDI at the country level and the performance of companies.

According to Beugelsdijk and Mudambi (2013), multinationals may benefit from those internal institutional and economic differences, seeking subnational regions where there is a correspondence between potential customers and the offers of products and services. The cash deposits may be used to finance competitive strategies which, in their turn, may improve performance (FRESARD, 2010).

Such strategies include decisions about capital expenditures, research and development expenditures, the location of stores or factories, distribution networks, the use of advertising directed against competitors, the recruitment of more productive workers, or the acquisition of key suppliers or business partners. (CAMPELLO, 2006; FRESARD, 2010).

Fresard (2010) found strong evidence that a company's cash stock is associated with the market expansion process, demonstrating that companies with greater cash reserves expand their market shares more than their competitors, revealing an economic effect important of the cash.

Companies with growth opportunities have a greater need for cash (ROCCA et al., 2019). Previous studies (for example, OPLER et al., 1999) show that growth opportunities are associated with liquidity, those studies supported the cash precautionary motive to reduce the likelihood of financial difficulties (ROCCA et al., 2019). Rocca et al. (2019) demonstrated that the relation between cash and performance is positively moderated by growth opportunities, understood as the increase in the company's business.

In the Brazilian context, for example, Forti et al. (2011) found a positive linear relation between cash retention and operational performance and concluded that the retention of large volumes of cash may be considered a viable competitive strategy for companies, with positive effects on performance.

In the present research, as representative variables of the determinants of the location of the subnational regions, we understand that the market size and the level of municipal sustainable development (measured by the Cities Sustainable Development Index – CSDI-BR, presented in the next section) of the subnational region in which the company operates influence its performance. Based on what has been exposed, we defend the interaction of cash with the determinants of the location of subnational regions is related to performance according to the location of the subsidiary(ies).

By examining the relation between location determinants and the performance of subsidiaries located in subnational regions of Latin America countries, Oliveira (2020) did not analyze the interaction of specific features at the company level with the location determinants of subnational regions, in this research represented by market size and CSDI -BR.

In addition, the author took into account the state level to analyze the effects of location determinants, but it is argued that the state itself has internal social and economic differences that may influence the performance of companies. The state of Minas Gerais, by way of illustration, is a federal entity characterized by social and economic heterogeneity, with economically distinct regions, such as Triângulo Mineiro and Vale do Jequitinhonha.

For this purpose, this research investigates whether the determinants of the location of subnational regions (market size and CSDI-BR) at the city level of location of the subsidiary(ies) of Brazilian companies listed on B3, interacted with the cash, have an effect on its consolidated performance.

In view of the above, the following hypotheses are presented:

H1: The interaction between cash and the sustainable development index of the municipality where the subsidiary of Brazilian companies is located is related to its performance.

H2: The interaction between cash and the market size of the municipality where the subsidiary of Brazilian companies is located is related to its performance.

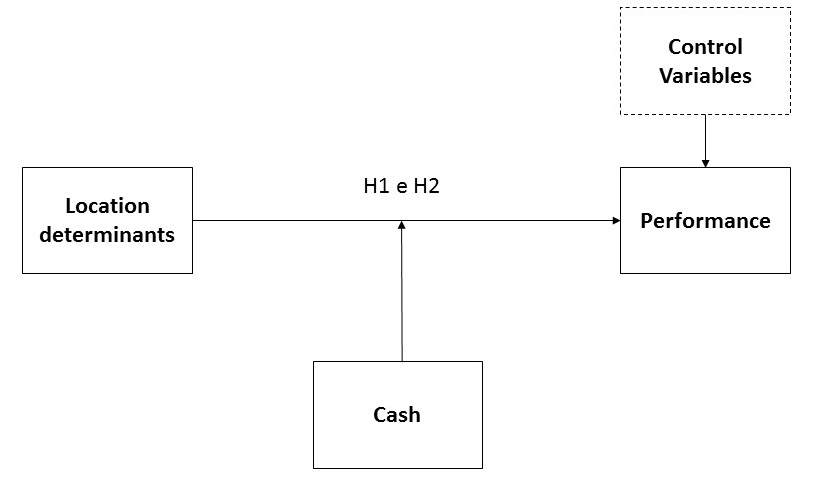

Figure 1 presents the conceptual model of the effect of location determinants on firm performance moderated by cash reserves.

Figure 1 - Determinants of subnational region location, cash and performance: a conceptual model

Source: Prepared by the authors (2021)

The model presented in Figure 1 proposes, therefore, that the interaction of cash with the determinants of location in subnational regions (market size and CSDI-BR) influences the performance of Brazilian companies.

The initial sample of 353 Brazilian companies listed on B3 was based on accounting data collected from the Economática database for the year 2020. There were excluded 158 companies from section K, divisions 64 to 66 of the National Register of Economic Activities – NREA version 2.0, which perform activities called financial activities, insurance and related services, resulting in a final sample of 195 companies from the following sectors: agriculture, extractive industry, transformation industry, electricity and gas, trade and preparation of motor vehicles, transport and warehousing, food, information and communication, real estate construction and leasing. The year 2020 was defined due to the availability of data on the location determinants of subnational regions and data on the location of the headquarters and subsidiaries of companies.

Data related to the determinants of the location of subnational regions were collected from the BIGS-Cities (Brazilian Institute of Geography and Statistics) database, referring to the city's population, from the Sustainable Cities Institute database, referring to the Sustainable Development Index of Cities (SDIC-BR), the Federal Revenue database pertaining to the location data of the headquarters and the TradeMap database in relation to the location data of the subsidiaries.

The CSDI-BR is an index developed under the Sustainable Cities Program (SCP), whose methodology was developed by the Sustainable Development Solution Network (SDSN), being an initiative of the United Nations (UN) to bring together technical and scientific knowledge from academia, civil society and the private sector in support of solutions at local, national and global scales (CSDI, 2021).

The CSDI-BR comprises 88 indicators related to various areas of public administration, calculated based on data from official sources, such as the BIGS itself (CSDI, 2021). The Index is made up of 17 Sustainable Development Goals (SDGs), for example, quality of education, decent work and economic growth, peace, justice and effective institutions (CSDI, 2021) and the score given to the city ranges from 0 to 100, the closer to 100, the closer the municipality is to the optimal performance regarding its sustainable development, comprising the socio-cultural, economic, environmental and political-institutional dimensions of the municipality in a single index.

The most recent version refers to the year 2020, which comprises the evolution of municipal indicators from 2010 to 2019. To analyze the effect of CSDI-BR on company performance, following Farole et al. (2017), ideally, the index should be measured before the period to be analyzed referring to the companies' accounting data, therefore, the analysis of data at the company level for the year 2020 is justified.

The variables are from consolidated and year-end balance sheets and income statements. Table 1 lists the variables used in the study.

Table 1 - Variables of the study of regional diversification

|

Variable |

Acronym |

Definition |

Database |

Authors |

|

|

Dependent |

|||||

|

Financial performance |

ROE |

Net income divided by equity |

Economatics |

Oliveira (2020) |

|

|

Operational performance |

ROA |

Operating earnings before interest are divided by total assets. |

|||

|

Independent |

|||||

|

Subnational market size |

POP |

The population of the subnational region |

BIGS |

|

|

|

Sustainable headquarters development |

CSDI |

Cities Sustainable Development Index |

CSDI-BR |

Rahman (2022) |

|

|

Cash retention |

CAS |

Cash and cash equivalents divided by total assets |

Economatics |

Forti , Peixoto and Freitas (2011); Jung, Foege and Nuesch (2020); Pereira Junior, Pereira and Penedo (2021) |

|

|

Control |

|||||

|

Firm growth |

GRO |

Natural logarithm of the ratio of sales (t) – sales (t-1) |

Economatics |

Jung, Foege and Nuesch (2020); Pereira Júnior, Pereira and Penedo (2021); |

|

|

Leverage |

LEV |

Total debt divided by total assets |

Jung, Foege and Nuesch (2020); Pereira, Pereira and Penedo (2021) |

||

|

Firm size |

SIZ |

Natural logarithm of total assets |

Rocca and Cambrea (2018); Pereira, Pereira and Penedo (2021) |

||

Source: Prepared by the authors (2021)

In order to avoid scaling problems, the POP variable was transformed by dividing the data by 1,000,000. For sample companies that have subsidiaries in more than one city, the CSDI and POP of the subsidiary's location were calculated based on the average of the development index and population of the cities where the subsidiaries are located.

The study variables were winsorized at 1% in each band to treat the influence of outliers. Test results for Variance Inflation Factors (VIFs) ranged between 1.22 and 1.72, below the critical limits of multicollinearity. Aiming to verify the existence of heteroscedasticity, the Wald test was performed, which demonstrated that the models presented problems of heteroscedasticity, so the regressions were run considering standard errors robust to heteroscedasticity and grouped at the level of the city where the headquarters are located and the city of origin company's subsidiary. The sector effect was addressed through a sector dummy.

The table 1 shows the list of the 10 (ten) cities with the largest and smallest population (market size) and with the largest and smallest CSDI (sustainable development) in which the companies in the sample are headquartered.

Table 1 – The ten cities with the largest and smallest population and CSDI – headquarters location

|

Cities with the largest population (in thousands) |

Cities with the smallest population (in thousands) |

|

||

|

City |

Population |

City |

Population |

|

|

Sao Paulo-SP |

12,325.23 |

Don't Touch Me – RS |

17.76 |

|

|

Rio de Janeiro - RJ |

6,747.82 |

Pradopolis – SP |

21.87 |

|

|

Brasilia DF |

3,055.15 |

Four Bars – PR |

23.91 |

|

|

Salvador BA |

2,886.70 |

São Sebastião do Caí – RS |

25.96 |

|

|

Fortaleza – EC |

2,686.61 |

Fraiburgo – SC |

36.58 |

|

|

Belo Horizonte – MG |

2,521.56 |

Tijucas – SC |

39.16 |

|

|

Manaus – AM |

2,219.58 |

Pojuca – BA |

39.97 |

|

|

Curitiba – PR |

1,948.63 |

Eldorado do Sul – RS |

41.90 |

|

|

Recife PE |

1,653.46 |

Timbo – SC |

44.98 |

|

|

Goiania - GO |

1,536.10 |

Viana - ES |

52.65 |

|

|

Cities with greater sustainable development |

Cities with less sustainable development |

|

||

|

City |

CSDI |

City |

CSDI |

|

|

São Caetano do Sul – SP |

69.30 |

Eldorado do Sul – RS |

44.51 |

|

|

Jundiaí – SP |

67.09 |

Bethlehem – PA |

46.74 |

|

|

Indaiatuba – SP |

66.88 |

Magé – RJ |

49.76 |

|

|

Jaraguá do Sul – SC |

66.08 |

São Luís – MA |

49.81 |

|

|

Curitiba – PR |

66.03 |

Camaçari – BA |

50.08 |

|

|

Piracicaba – SP |

65.36 |

Eusébio – CE |

50.34 |

|

|

Barueri – SP |

65.34 |

Viana – ES |

51.37 |

|

|

Franca – SP |

65.23 |

Pojuca – BA |

51.37 |

|

|

Sao Paulo-SP |

64.86 |

Natal, RN |

51.47 |

|

|

Florianópolis - SC |

64.15 |

Embu das Artes - SP |

51.90 |

|

Source: Prepared by the authors (2021)

It is observed in Table 1 that of the cities in the sample where the studied companies are headquartered, São Paulo and Não-Me-Toque are the ones with the largest and smallest market size, respectively. Also, the cities of São Caetano do Sul and Eldorado do Sul are the cities with the highest and lowest levels of sustainable development.

The table 2 shows the relation between the 10 (ten) cities with the largest and smallest population (market size) and with the largest and smallest CSDI (sustainable development) in which the sample companies have subsidiary(s).

Table 2 - The ten cities with the largest and smallest population and CSDI - location of the subsidiary

|

Cities with the largest population (in thousands) |

Cities with the smallest population (in thousands) |

||

|

City |

Population |

City |

Population |

|

Sao Paulo-SP |

12,325.23 |

Vargem Bonita - MG |

2.148 |

|

Rio de Janeiro - RJ |

6,747.82 |

Santa Efigênia de Minas – MG |

4,381 |

|

Brasilia DF |

3,055.15 |

Motuca – SP |

4,795 |

|

Salvador BA |

2,886.70 |

Gavião Peixoto – SP |

4.815 |

|

Fortaleza – EC |

2,686.61 |

Tasso Fragoso – MA |

8,582 |

|

Belo Horizonte – MG |

2,521.56 |

Maydidate – RS |

9,647 |

|

Manaus – AM |

2,219.58 |

Ouroeste – SP |

10,539 |

|

Curitiba – PR |

1,948.63 |

Jaguari – RS |

10,760 |

|

Recife PE |

1,653.46 |

Palmares do Sul – RS |

11,330 |

|

Goiania - GO |

1,536.10 |

Lages - SC |

11,344 |

|

Cities with greater sustainable development |

Cities with less sustainable development |

||

|

City |

CSDI |

City |

CSDI |

|

São Caetano do Sul – SP |

69.30 |

Macapá - AP |

43.35 |

|

Valinhos – SP |

68.97 |

São Lourenço da Mata – PE |

43.55 |

|

Limeira – SP |

68.89 |

Marituba – PA |

43.80 |

|

Jundiaí – SP |

67.09 |

Ipojuca – PE |

44.45 |

|

Indaiatuba – SP |

66.88 |

Eldorado do Sul – RS |

44.51 |

|

Santos – SP |

66.58 |

Porto Velho – RO |

46.13 |

|

Jaguariúna – SP |

66.09 |

Bethlehem – PA |

46.74 |

|

Jaraguá do Sul – SC |

66.08 |

Queimados – RJ |

46.89 |

|

Curitiba – PR |

66.03 |

Horizon - CE |

47.91 |

|

Piracicaba - SP |

65.37 |

São Gonçalo do Amarante - CE |

47.99 |

Source: Prepared by the authors (2021)

According to Table 2, of the sample cities in which the companies studied have a subsidiary(ies), São Paulo and Vargem Bonita are the ones with the largest and smallest market size, respectively. The cities of São Caetano do Sul and Macapá are the cities with the highest and lowest levels of sustainable development.

Table 3 shows the distribution of the number of companies and cities by mesoregion where the sample companies are headquartered and also where they have subsidiary(s).

Table 3 - Distribution of companies by Brazilian mesoregions

|

|

Headquarters location |

Subsidiary location |

|||

|

Mesoregion |

State |

Number of cities |

Number of headquarters |

Number of cities |

Number of subsidiaries |

|

Acre Valley |

AC |

|

|

1 |

1 |

|

Amazon Center |

AM |

1 |

1 |

1 |

12 |

|

East Alagoas |

AL |

|

|

1 |

6 |

|

South of Amapá |

AP |

|

|

1 |

3 |

|

Central-North Bahia |

BA |

|

|

1 |

1 |

|

Central-South Bahia |

|

|

3 |

3 |

|

|

metropolitan of Salvador |

3 |

7 |

5 |

9 |

|

|

South Bahia |

|

|

2 |

2 |

|

|

Metropolitan of Fortaleza |

CE |

2 |

3 |

4 |

9 |

|

Federal District |

DF |

|

|

1 |

4 |

|

Central Espírito Santo |

ES |

1 |

1 |

4 |

4 |

|

Goiás Center |

GO |

|

|

2 |

6 |

|

East Goiás |

|

|

1 |

1 |

|

|

North Goiás |

|

|

1 |

1 |

|

|

south Goiás |

|

|

1 |

1 |

|

|

Maranhense Center |

MA |

|

|

1 |

1 |

|

North Maranhão |

1 |

1 |

1 |

4 |

|

|

South Maranhão |

|

|

1 |

1 |

|

|

Central Mining |

MG |

|

|

1 |

1 |

|

Belo Horizonte Metro |

3 |

15 |

7 |

21 |

|

|

north of mines |

1 |

1 |

1 |

1 |

|

|

west of mines |

1 |

1 |

1 |

1 |

|

|

South and Southwest of Minas Gerais |

|

|

1 |

1 |

|

|

Triângulo Mineiro and Alto Paranaíba |

|

|

3 |

4 |

|

|

Rio Doce Valley |

|

|

1 |

1 |

|

|

Wood zone |

1 |

1 |

1 |

2 |

|

|

Central-North of Mato Grosso do Sul |

MS |

|

|

1 |

2 |

|

Southwest of Mato Grosso do Sul |

|

|

1 |

1 |

|

|

Southeast Mato Grosso |

MT |

1 |

1 |

|

|

|

Center-South Mato Grosso |

1 |

1 |

1 |

2 |

|

|

Northeast Mato Grosso |

|

|

1 |

1 |

|

|

North Mato Grosso |

|

|

2 |

2 |

|

|

Belem subway |

PA |

1 |

1 |

2 |

6 |

|

Agreste Paraíba |

PB |

|

|

1 |

1 |

|

Paraiba Forest |

|

|

1 |

2 |

|

|

Agreste Pernambuco |

PE |

|

|

1 |

1 |

|

Metropolitana do Recife |

1 |

3 |

5 |

6 |

|

|

Central-North Piauiense |

PI |

|

|

1 |

1 |

|

North of Piauí |

|

|

1 |

1 |

|

|

Metropolitan of Curitiba |

PR |

2 |

4 |

3 |

13 |

|

Eastern Center of Paraná |

1 |

1 |

1 |

1 |

|

|

North Central Paraná |

1 |

1 |

2 |

5 |

|

|

Metropolitan of Rio de Janeiro |

RJ |

4 |

30 |

6 |

43 |

|

North Fluminense |

|

|

1 |

3 |

|

|

South Fluminense |

|

|

1 |

3 |

|

|

East Potiguar |

RN |

1 |

2 |

2 |

5 |

|

east rondoniense |

RO |

|

|

1 |

1 |

|

Madeira-Guaporé |

|

|

1 |

1 |

|

|

West Center Rio Grande |

RS |

|

|

1 |

1 |

|

Metropolitan of Porto Alegre |

6 |

9 |

10 |

19 |

|

|

Northeast Rio Grande |

1 |

4 |

2 |

5 |

|

|

Northwest Rio Grande |

1 |

1 |

2 |

2 |

|

|

Southeast Rio Grande |

|

|

3 |

3 |

|

|

East Sergipe |

SE |

|

|

1 |

3 |

|

backlands of Sergipe |

|

|

1 |

1 |

|

|

Greater Florianopolis |

SC |

2 |

3 |

2 |

8 |

|

North of Santa Catarina |

2 |

4 |

3 |

6 |

|

|

Serrana |

|

|

1 |

2 |

|

|

south of Santa Catarina |

|

|

2 |

2 |

|

|

Itajai Valley |

1 |

4 |

2 |

4 |

|

|

Araçatuba |

SP |

|

|

2 |

1 |

|

Araraquara |

|

|

3 |

2 |

|

|

Campinas |

4 |

4 |

10 |

14 |

|

|

Macro Metropolitan Paulista |

1 |

1 |

5 |

8 |

|

|

Sao Paulo Metropolitan |

9 |

84 |

15 |

90 |

|

|

Piracicaba |

1 |

1 |

4 |

4 |

|

|

Presidente Prudente |

|

|

1 |

1 |

|

|

Ribeirão Preto |

2 |

2 |

5 |

5 |

|

|

São Jose do Rio Preto |

1 |

1 |

1 |

2 |

|

|

Paraíba Paulista Valley |

2 |

2 |

3 |

4 |

|

|

East of Tomaytins |

TO |

|

|

1 |

1 |

|

Total |

|

60 |

195 |

164 |

390 |

Source: Prepared by the authors (2021)

It may be seen in Table 3 that the 195 headquarters of the companies in the sample are distributed in 60 different cities, while the 390 subsidiaries are in 164 different cities, 71 mesoregions and 26 Brazilian states. The mesoregions with the largest number of headquarters and subsidiaries are Metropolitana de São Paulo and Metropolitana do Rio de Janeiro.

The table 4 shows the results of data regressions for the sustainable development index and population of the headquarters/subsidiary city of the companies and cities grouped in a cluster. The specifications of the variables may be seen in Chart 1. The coefficients, the constant and the adjusted R 2 for each regression are shown.

Table 4 - Results of the regressions referring to the location of the headquarters and subsidiary

|

|

|

Headquarter Location |

Subsidiary Location |

||

|

Dependent |

|

ROA |

ROE |

ROA |

ROE |

|

|

Mod. 1 |

Mod. 2 |

Mod. 3 |

Mod. 4 |

|

|

Growth |

|

4.84 |

59.0* |

2.85 |

50.6*** |

|

Leverage |

|

-27.7** |

-86.6* |

-14.8*** |

-2.15 |

|

Size |

|

7.01*** |

7.27 |

5.65* |

-9.24 |

|

Population_Headquarters |

|

-0.88*** |

0.51 |

|

|

|

CSDI_Headquarters |

|

0.41* |

-1.47 |

|

|

|

Population_Subsidiary |

|

|

|

-1.11** |

0.44 |

|

CSDI_Subsidiary |

|

|

|

2.41 |

0.05 |

|

Cash |

|

|

|

3.72 |

0.46 |

|

Population_Subsidiary*Cash |

|

|

|

-1.63 |

-2.20*** |

|

CSDI_Subsidiary*Cash |

|

|

|

3.33 |

5.16 |

|

_cons |

|

-56.6*** |

-14.7 |

-26.4 |

77.6 |

|

VIF |

|

1.22 |

1.24 |

1.64 |

1.72 |

|

No |

|

176 |

150 |

137 |

119 |

|

R 2 Adjusted |

|

0.32 |

0.13 |

0.28 |

0.13 |

Source: Prepared by the authors (2021)

Note: Coefficient = beta coefficient or regressor parameter. ROA = Operating performance; ROE = Financial performance; CSDI = Sustainable Development Index.

*, **, *** = p < 0.10, p < 0.05, p < 0.01, respectively.

Regarding the results according to the location of the companies' headquarters, Table 4 shows that market size (population of the headquarters city) is negatively associated with operational performance (β = -0.88, p. < 0.01) and that the sustainable development index of the host city is positively associated with the operational performance (β = 0.41, p. < 0.10) of the companies in the sample. The results suggest that companies headquartered in cities with smaller market sizes and greater sustainable development had a better operational performance, that is, the smaller the market size and the greater the city's development, the greater the performance. The results suggest that policies that improve sustainable development goals in less-developed regions may benefit the performance of companies located in those regions (FAROLE et al., 2017).

Regarding the results according to the location of the subsidiary(ies), the Table 4 shows that moderation of cash with the market size is significant and negative (β = -2.20, p. < 0.01). Those results imply that the company that has a subsidiary(ies) in cities with smaller market sizes and a higher level of cash has a positive effect on financial performance, which confirms H2 and rejects hypothesis H1.

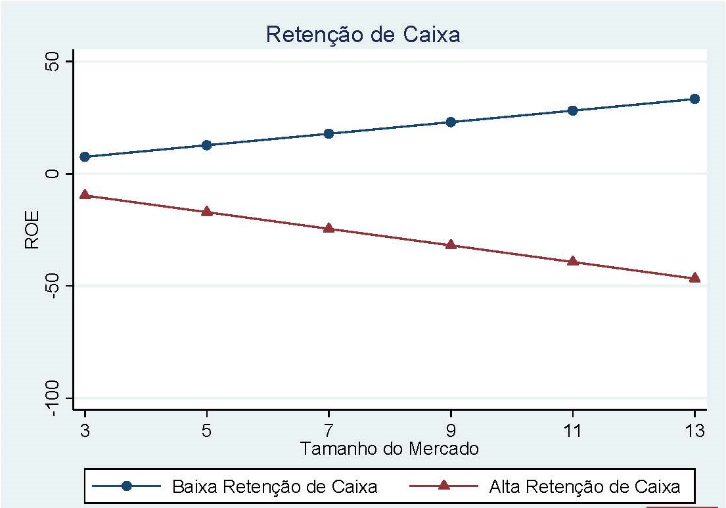

That is also represented in the graph in Figure 2 if cash retention is high.

Figure 2 - Moderating effects of the company's cash retention

Source: Prepared by the authors (2021)

Note: The plot was generated using the margins and margins plot command in STATA. Shows company performance (vertical axis) as measured by ROE in relation to the market size (horizontal axis). The limits apply to the rounded minimum and maximum value of the city's population. The 1st and 99th percentiles of the moderating variable were used as indications for lower and upper cash retention.

It is observed in the graph of Figure 2 that cash weakens the relation between market size and performance of the companies in the sample, due to the signs of the predictor (Population_Subsidiary) and the interaction term (Population_Subsidiary*Cash) being different, being one positive and the other negative. The relation between market size and performance weakens as cash levels increase, suggesting that companies that have subsidiary(s) in cities with smaller market sizes and maintain higher cash levels may be associated with better performance.

It is suggested that cash assumes a strategic role in the context of regional diversification in which the company has a subsidiary(s) in smaller markets for a positive effect on performance. According to Fresard (2010), the company rich in cash in competitive markets may use cash retention to finance competitive strategies such as the location of stores or factories, and efficient distribution networks, which, in its turn, have a positive effect on performance.

Also according to Fresard (2010), the strategic value of money assumes a preventive dimension of restricting the entry of potential competitors and distorting their investment decisions, increasing the market share of the company rich in cash. It is believed, therefore, that in smaller markets competition is more pronounced and cash may be a strategic resource that contributes to better financial performance.

In the opposite direction, cash decreases its strategic value in larger markets, suggesting that the costs related to familiarization with environmental factors may be compensated with a high sales volume (MATALONI, 2011), and it is possible that larger markets exert less competitive pressures and, therefore, cash is not strategic as in smaller markets to improve performance.

The objective of this study was to verify whether the interaction of cash with the location determinants of the subnational regions of the subsidiary's city influences the performance of Brazilian companies listed on B3, according to the location of its subsidiary(ies), referring to the year 2020. Data analysis was performed using multiple linear regressions using the Generalized Least Squares (GLM) method.

Complementarily, we sought to identify whether the location determinants of the subnational regions where companies are headquartered are associated with the performance of Brazilian companies listed on B3.

The results show that the interaction between cash and the market size of the subsidiary's location city is related to financial performance, as well as the market size and the sustainable development of the company's headquarters location are negatively and positively associated, respectively, with the operational performance of the companies in the sample.

This study suggests that liquidity has strategic value for companies in the process of business expansion. Managers of companies that diversify regionally should analyze the costs and benefits of liquidity since it assumes a strategic value according to the size of the market where its subsidiary(ies) is(are) located.

In addition, regarding the process of choosing the company's headquarters, it is suggested that managers take into account sustainable development and the size of the market where the company will develop its activities since the results indicate that more profitable companies are headquartered in regions more developed.

As a limitation of the research, the results are limited to Brazilian companies listed on B3, being the present study of limited generalization. It is suggested that future research investigate whether the results of this study are valid for unlisted companies, as well as for small and medium-sized companies.

Another limitation that may be raised is the temporal aspect of the research since the present paper analyzed data referring to the year 2020, and it is not possible to establish any causality, as the results only show a correlation. Therefore, we recommend future researches study the effects of the cities' sustainable development index on performance over time.

Finally, also as a limitation of the research, it is highlighted that it was not possible to relate the determinants of the location of the subnational regions with the performance of the subsidiary itself due to the fact that the performance data of the companies are only available on a consolidated basis.

ALMEIDA, H.; CAMPELLO, M.; CUNHA, I.; WEISBACH, M. Corporate Liquidity Management: A Conceptual Framework and Survey. Annual Review of Financial Economics, v. 6, p. 135-162, 2014.

AMITI, M.; JAVORCIK, B. Trade costs and location of foreign firms in China. Journal of Development Economics, vol. 85, no. 1–2, p. 129–149, 2008.

BARNEY, JB Firm resources and sustained competitive advantage. Journal of Management, vol. 17, no. 1, p. 99-120, 1991.

BEUGELSDIJK, S.; MUDAMBI, R. MNEs as border-crossing multi-location enterprises: the role of discontinuities in geographic space. Journal of International Business Studies, v. 44, p. 413-426, 2013.

CAMPELLO, M. Debt financing: Does it boost or hurt firm performance in product markets? Journal of Financial Economics, v. 82, no. 1, p. 135–172. doi:10.1016/j.jfineco.2005.04.001.

CASTELLANI, D.; GIANGASPERO, G.; ZANFEI, A. Heterogeneity and distance. Some propositions on how differences across regions, firms and functions affect the role of distance in FDI location decisions. Working Papers Series in Economics, Mathematics and Statistics, 2013.

CHAN, CM; MAKINO, S.; ISOBE, T. Does sub-national region matter? Foreign affiliate performance in the United States and China. Strategic Management Journal, vol. 31, no. 11, p. 1226–1243, 2010.

CHIDLOW, A.; HOLMSTROM-LIND, C.; HOLM, U.; TALLMAN, S. Do I stay or do I go? Sub-national drivers for post-entry subsidiary development. International Business Review, vol. 24, no. 2, p. 266–275, 2015.

DRAZIN, R.; VAN de VEN, AH Alternative forms of fit in contingency theory. Administrative Science Quarterly, vol. 30, no. 4, p. 514–539, 1985. https://doi.org/10.2307/2392695.

DUNNING, JH Location and the multinational enterprise: a neglected factor? Journal of International Business Studies, vol. 29, no. 1, 45–66, 1998. https://doi.org/10.1057/palgrave.jibs.8490024 .

FAROLE, T.; HALLAK, I, HARASZTOSI, P.; TAN, S. Business Environment and Firm Performance in European Lagging Regions. policy Research Working Paper 8281 – World Bank Group, 2017.

FORTI, CAB; PEIXOTO, MF; FREITAS, SK Cash retention, operating performance and value: a study in the Brazilian capital market. Accounting and Organizations Magazine, v. 5, no. 13, p. 20-33, 2011.

FRESARD, L. Financial Strength and Product Market Behavior: The Real Effects of Corporate Cash Holdings. Journal of Finance, vol. 65, no. 3, p. 1097-1122, 2010. https://doi-org.ez34.periodicos.capes.gov.br/10.1111/j.1540-6261.2010.01562.x.

GIL, AC; OLIVA, E. de C.; SILVA, EC da. Development of regionality: new field of administration. ANPAD MEETING, v. 31, p. 1-13, 2007.

HSU, C.; CHEN, H.; CASKEY, D. Local conditions, entry timing, and foreign subsidiary performance. International Business Review, vol. 26, no. 3, p. 544–554, 2017.

HUTZSCHENREUTERA, T.; MATTA, T.; KLEINDIENSTB, I. going subnational: a literature review and research agenda. Journal of World Business, v. 55, no. 4, 2020.

CSDI. SUSTAINABLE DEVELOPMENT INDEX OF CITIES - BR. https://CSDI-br.sdgindex.org/

JUNG, C.; FOEGE, JN; NEUSH, S. Cash for contingencies: How the organizational task environment shapes the cash-performance relation. Long Range Planning, v. 53, no. 3, 2020. https://doi.org/10.1016/j.lrp.2019.05.005 .

LUO, YD; PARK SH Strategic alignment and performance of market-seeking MNCs in China. Strategic Management Journal, vol. 22, no. 2, p. 141–155, 2001.

MA, X.; TONG, TW; FITZA, M. How much does subnational region matter to foreign subsidiary performance? Evidence from Fortune Global 500 Corporations' investment in China. Journal of International Business Studies, vol. 44, p. 66–87, 2013. doi:10.1057/jibs.2012.32.

MATALONI, RJ The structure of location choice for new US manufacturing investments in Asia-Pacific. Journal of World Business, vol. 46, no. 2, p. 154–165, 2011.

MEYER, KE; NGUYEN, HV Foreign investment strategies and sub-national institutions in emerging markets: Evidence from Vietnam. Journal of Management Studies, vol. 42, no. 1, p. 63–93, 2005. https://doi.org/10.1111/j.1467-6486.2005.00489.x.

OLIVEIRA, D. da S. The effects of subnational location determinants on institutional distance and subsidiary performance. Thesis (Doctorate in Management and Regionality) – Municipal University of São Caetano do Sul. São Caetano do Sul, 2020. 130f.

OPLER, T.; PINKOWITZ, L.; STULZ, R.; WILLIAMSON, R. The determinants and implications of corporate cash holdings. Journal of Financial Economics, v. 52, p. 3-46, 1999. https://doi.org/10.1016/S0304-405X(99)00003-3.

PENROSE, ET The theory of the growth of the firm. Wiley, New York, NY. 1959.

PEREIRA JUNIOR, A.; PEREIRA, VS; PENEDO, AST The effect of cash and investment retention on the operating performance of Brazilian exporting and domestic companies in periods of economic growth and recession. Contemporary Accounting Magazine, v. 18, no. 46, p. 148-162, 2021. https://doi.org/10.5007/2175-8069.2021.e73580 .

RAHMAN, M. The effect of taxation on sustainable development goals: evidence from emerging countries. Heliyon, n. 8, 2022. https://doi.org/10.1016/j.heliyon.2022.e10512.

ROCCA, LM; CAMBREA, DR The effect of cash holdings on firm performance in large Italian companies. Journal of International Financial Management & Accounting, v. 30, p. 30-59, 2018. DOI: 10.1111/jifm.12090.

ROCCA, LM; STAGLIANO, R.; ROCCA, T.; CARIOLA, A.; SKATOVA, E. Cash holdings and SME performance in Europe: the role of firm-specific and macroeconomic moderators. Small Bus Econ, v. 53, p. 1051–1078, 2019. https://doi-org.ez34.periodicos.capes.gov.br/10.1007/s11187-018-0100-y .

SALAH, W. The impact of country-level and firm-level on financial performance: a multilevel approach. International Journal of Accounting, v. 6, no. 2, p. 41-53, 2018.

SLANGEN, AHL The comparative effect of subnational and nationwide cultural variation on subsidiary ownership choices: the role of spatial coordination challenges and penrosean growth constraints. Economic Geography, v. 92, no. 2, p.145–171. https://doi.org/10.1080/00130095.2015.1096196 .

SUN, SL; PENG, MW; LEE, PR; TAN, W. Institutional open access at home and outward internationalization. Journal of World Business, v. 50, no. 1, p. 234–246, 2015. https://doi.org/10.1016/j.jwb.2014.04.003 .

TENG, L.; HUANG, D.; PAN, Y. The Performance of MNE Subsidiaries in China: Does It Matter to Be Close to the Political or Business Hub? Journal of International Management v. 23, no. 3, p. 292–305, 2017.

WANG, G.; SINGH, P. The evolution of CEO compensation over the organizational life cycle: A contingency explanation. Human Resource Management Review, v. 24, no. 2, p. 144-159, 2014. https://doi.org/10.1016/j.hrmr.2013.11.001 .

WERNERFELT, B. A resource-based view of the firm. Strategic Management Journal, vol. 5, 171-180, 1984. https://www.jstor.org/stable/2486175 .